You set aside pre-tax money. You forgot about it. Now December is approaching and you're panic-buying a thermometer you don't need. This is not a spending problem. It's a systems problem, and it's fixable before it happens again.

Let's talk about what actually works — and what the rules actually say, because most people have at least one of them wrong.

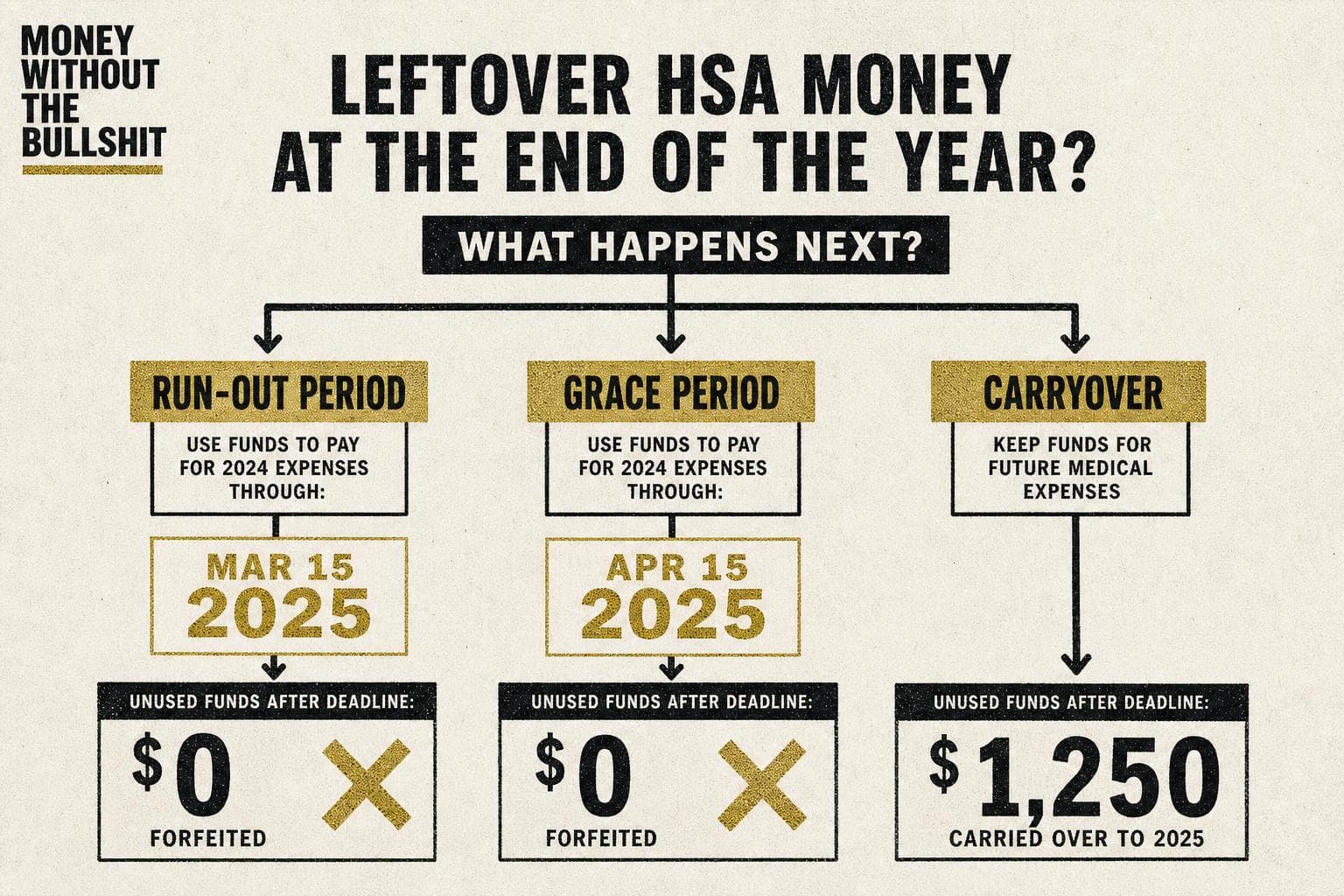

First, Know Which Deadline You're Actually Fighting

The "use it or lose it" rule is real, but it's not as binary as it sounds. Your FSA may have one of three structures, and confusing them is where people lose money.

A run-out period is not extra spending time — it's extra paperwork time. As LegalClarity explains, if you had a dental cleaning in November and never submitted the receipt, the run-out period (typically 90 days after your plan year ends) lets you file that claim. The expense had to happen during the plan year. A new appointment in February doesn't count, no matter how much money is left.

A grace period is different: it actually extends your spending window by up to two and a half months after the plan year ends. New expenses incurred during that window can be paid from last year's balance. If your plan year ends December 31 and your employer offers the full grace period, a March 1 doctor visit can still come out of your 2025 FSA funds — per LegalClarity.

A carryover rolls unused funds forward. For the 2026 plan year, the IRS allows plans to carry over up to $680 into 2027, per Revenue Procedure 2025-32. Anything above that threshold is forfeited. Your employer can set a lower limit but not a higher one.

Check your Summary Plan Description — your employer chooses which of these options to offer, and they are not required to offer any of them. Most people have no idea which structure their plan uses until they've already lost money.

The Actual Spending Strategies That Work

Once you know your deadline, the goal is to spend on things you'd buy anyway — not to manufacture medical expenses.

Schedule the appointments you've been putting off. Dental cleanings, eye exams, prescription refills, dermatology checks — these are real expenses you'll incur eventually. Scheduling them before your plan year ends converts future spending into current FSA spending. MedSurety recommends reviewing what specialist visits, dental work, and vision appointments you've been deferring, then front-loading them into the remaining plan year.

Stock up on OTC items you actually use. Since the CARES Act expanded FSA eligibility for over-the-counter medications (no prescription required), this category is broader than most people realize. Pain relievers, allergy medications, cold and flu remedies, and digestive health products all qualify under most plans, according to Vibe Blessings. So does SPF 15+ sunscreen and feminine hygiene items. If you'd buy these at CVS anyway, buying them with pre-tax FSA dollars is just a discount.

Consider durable medical equipment if you have a legitimate need. Braces, crutches, blood pressure monitors — these qualify and they're not cheap. If there's a real medical need in your household, this is the time to address it rather than deferring it into next year's out-of-pocket budget.

What doesn't work: buying things you'll never use just to zero out the balance. A $200 piece of equipment gathering dust in a closet isn't a win — it's just a different kind of waste.

Reality Check: "Just Max Out Your FSA Every Year"

This is the advice that sounds responsible and is often wrong.

An FSA is front-loaded — your full annual election is available on day one of the plan year, even if you haven't contributed that much yet. That's a real benefit if you have a major expense in January. But if you leave your job mid-year, you keep whatever you spent, even if your contributions haven't caught up. The employer eats that difference.

The flip side: if you overestimate your medical expenses and don't have a carryover option, you forfeit the excess. For the 2026 plan year, the FSA contribution limit is $3,400, per Revenue Procedure 2025-32 cited by Money.it. Electing the maximum without a realistic spending estimate is how people end up panic-buying in December.

The right FSA election is your expected medical spending, plus a small buffer if your plan has a carryover. Not the maximum. Not a round number you picked during open enrollment because it felt responsible.

The next step is simple: Log into your FSA portal today, check your balance and your plan's deadline structure, and list every medical expense you've been deferring. That list is your spending plan. Work through it before the clock runs out — not because you should feel guilty about leaving money on the table, but because it's already your money and the IRS already gave you the tax break on it.

Don't hand it back.