Most people pick their health insurance deductible the same way they pick a seat on an airplane — grab something that looks reasonable and stop thinking about it. The result is usually a low-deductible plan that costs more every month, chosen because high-deductible plans sound scary. That instinct is often wrong, and the math is simple enough to check in about ten minutes.

The Trade You're Actually Making

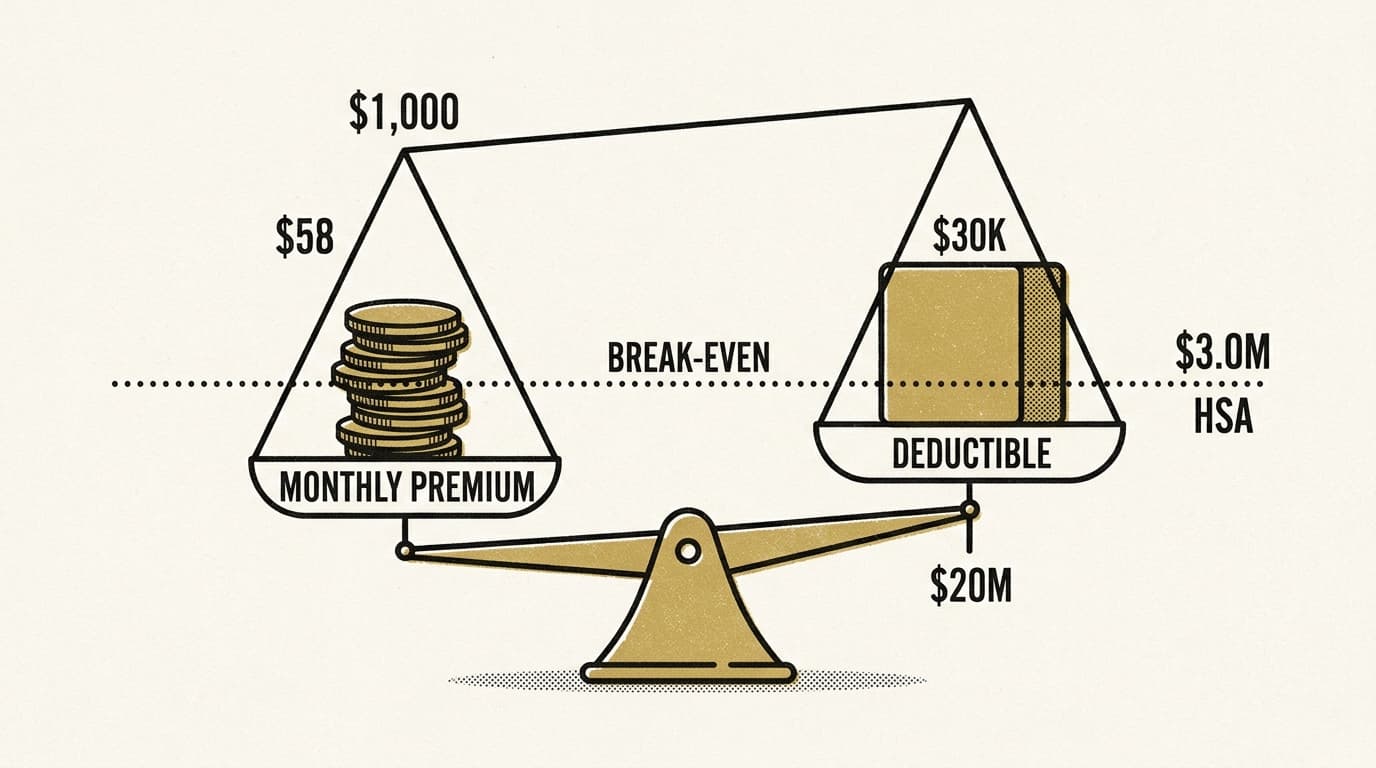

A deductible is a bet between you and your insurer. You're betting you'll need care. They're betting you won't. A high-deductible plan charges you less every month and more when something goes wrong. A low-deductible plan charges you more every month regardless.

The question isn't which one sounds safer. It's whether the monthly premium difference, multiplied across a year, exceeds what you'd realistically pay out-of-pocket under the higher deductible.

Here's the structure: take the annual premium difference between a low-deductible and high-deductible plan. That's your break-even number. If your actual medical spending in a typical year stays below that number, the high-deductible plan costs you less. If you regularly hit your deductible, the low-deductible plan wins.

Most healthy adults in their 20s and 30s who rarely see a doctor are paying a monthly premium tax to feel secure — and getting nothing back for it.

The HSA Changes the Math Significantly

High-deductible health plans (HDHPs) come with access to a health savings account, and that's where the math gets interesting. According to NPR/KFF Health News, HSAs are now available to people enrolled in lower-tier exchange plans including bronze and catastrophic coverage — a change many enrollees don't know about.

Money you put into an HSA is pretax. You can use it for qualified medical expenses, and — unlike a flexible spending account — it rolls over indefinitely. It's not a use-it-or-lose-it situation. For someone who doesn't spend it all in a given year, the HSA balance compounds. The high-deductible plan stops being just a cheaper monthly option and starts functioning as a tax-advantaged savings vehicle attached to your insurance.

That's a meaningful structural advantage. The premium savings fund the HSA. The HSA covers the deductible if you need it. In a good year, you come out ahead on both ends.

The catch: this only works if you actually fund the HSA. The teacher profiled in the NPR piece chose a bronze plan without knowing HSAs were an option. She's now sitting on a $5,800 deductible with no savings buffer. The plan isn't the problem — the missing piece is the account that makes it work.

When the Low-Deductible Plan Actually Wins

High-deductible plans aren't universally better. The assumptions matter.

If you have a chronic condition, take regular prescriptions, or anticipate a procedure — surgery, pregnancy, ongoing specialist visits — you'll likely hit your deductible every year. In that case, the monthly premium difference may not offset what you're paying out-of-pocket before coverage kicks in. Run the actual numbers for your situation, not the average.

The same logic applies if you don't have the cash cushion to absorb a large unexpected bill. A high-deductible plan with no HSA savings and no emergency fund is just a low-premium plan with a nasty surprise waiting. The math works in your favor over a full year, but only if you can survive the bad month when the bill arrives.

The New York Fed's recent analysis of homeowner's insurance contracts found that how people structure risk-sharing in insurance contracts reveals a lot about their actual financial resilience — not just their preferences. Choosing a deductible isn't just a cost optimization; it's a statement about what you can absorb. Be honest about that number.

Reality Check: "Lower Deductible = Better Coverage" Is Usually Wrong

The conventional wisdom is that a lower deductible means better insurance. It doesn't. It means you're pre-paying for coverage you may never use, at a premium set by an insurer who has better actuarial data than you do.

Better coverage means the plan actually covers what you need — the right network, the right drug formulary, the right out-of-pocket maximum. The deductible is one variable in that equation, not a proxy for quality. Conflating the two is how people end up overpaying for plans that still leave them exposed in the ways that matter.

The next step is concrete: Pull up your last two years of medical spending — what you actually paid, not what was billed. Compare that number to the annual premium difference between your current plan and the next-tier HDHP. If the premium savings exceed your typical out-of-pocket costs, you're probably on the wrong plan. Open an HSA the same week you switch.