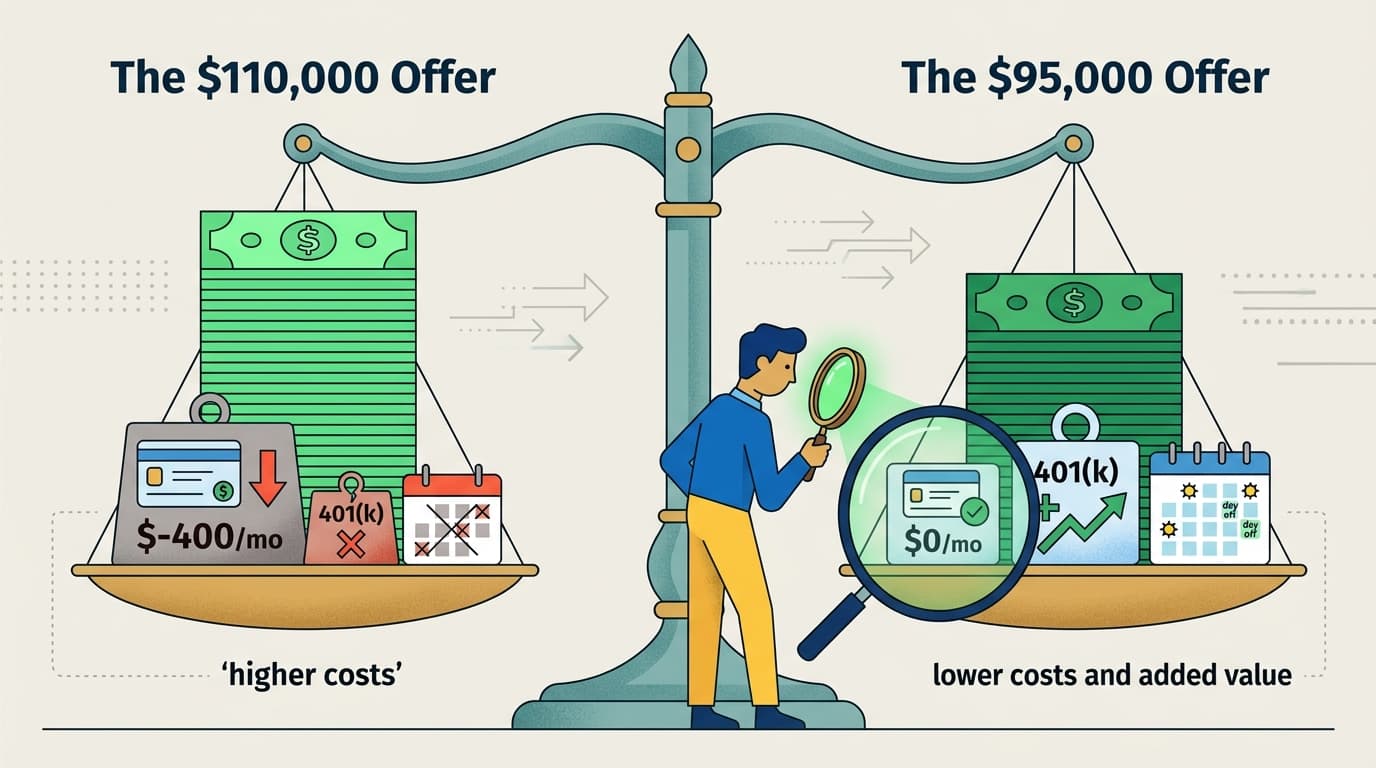

You get two offers. One pays $95,000, the other pays $110,000. The decision feels obvious — until you realize the higher-paying job requires you to cover $400/month in health insurance premiums. That's $4,800 a year. Suddenly the gap is $10,200, not $15,000. Factor in a worse 401(k) match and less PTO, and the "better" offer might actually cost you money.

This is the core problem with evaluating job offers: the salary number is legible, so we treat it as the whole answer. Everything else gets handwaved.

The Benefits Gap Is Usually Bigger Than You Think

First Alliance Credit Union frames it well: benefits are your "invisible paycheck." They affect your financial life without showing up on your pay stub, which makes them easy to ignore and expensive to underestimate.

Health insurance is the biggest variable. Two plans with the same monthly premium can have wildly different out-of-pocket maximums, deductibles, and network coverage. A plan that looks cheaper upfront can cost you thousands more in a bad year. Before you compare offers, get the actual plan documents — not the summary — and look at what you'd pay in a typical year, not just the best case.

Retirement matching is the other one people consistently undervalue. An employer that matches 4% of your salary is effectively adding 4% to your compensation, tax-advantaged. An employer that matches nothing is not. That difference compounds. Over a career, it's not a rounding error.

PTO, remote flexibility, equity, bonuses — these all matter too, but health and retirement are where the biggest dollar gaps hide.

Market Research Is Less Useful Than You Think

Here's the counterintuitive part: all that time you spend on Glassdoor and LinkedIn trying to figure out "the right number" is mostly wasted. According to a negotiation advisor who formerly worked at Salary.com — as reported by Business Insider — companies pay for sophisticated compensation data and then frequently ignore it anyway. Each firm has its own budget philosophy, and each team has its own constraints. Market data tells you a range. It doesn't tell you what this company, this team, this quarter can actually offer.

The most useful signal isn't research — it's a competing offer. If you have two offers simultaneously, you know exactly what the market thinks you're worth right now, in real conditions, not survey averages.

The Actual Framework: Build a Comparable Number

Stop comparing salaries. Start comparing total annual compensation, net of your costs.

For each offer, work through this:

- Base salary — the starting point, not the endpoint

- Employer health contribution — what are they covering, and what will you actually pay out of pocket in a normal year?

- Retirement match — what percentage, up to what cap, and when does it vest?

- Bonus structure — is it discretionary or formula-based? What did people actually receive last year?

- Equity or profit-sharing — if applicable, what's the vesting schedule and what's a realistic value?

Once you've run those numbers for both offers, you have something worth comparing. The gap between the headline salaries and the real gap is often surprising — sometimes the lower-salary offer wins outright.

Reality Check: "Never Negotiate — You Might Lose the Offer"

This fear is almost entirely unfounded, and it's costing people real money. Research from the Pew Research Center found that about 60% of U.S. workers didn't try to negotiate when they received a job offer. That's a lot of money left on the table based on a fear that rarely materializes.

The Harvard Program on Negotiation illustrates the compounding effect: a $15,000 difference in starting salary, with identical 3% annual raises over a career, produces over $1.5 million in lifetime earnings difference — including investment returns on the gap. That's not a motivational poster stat. That's arithmetic.

Companies expect negotiation. Rescinding an offer because someone asked for more is vanishingly rare. The actual risk of negotiating is low; the cost of not negotiating is permanent.

Once you've built your comparable number and identified which offer actually pays more, negotiate the one you want. You now have a real argument — not "I want more money," but "here's what the full compensation picture looks like and here's what I'm asking for." That's a different conversation.