Most people who hear "Roth conversion ladder" file it under "complicated tax stuff for people with too much money and time." That's a mistake. The core idea is simple: you have money in a pre-tax retirement account, you'll owe taxes on it eventually, and the question is when you pay those taxes and at what rate. The ladder is just a systematic answer to that question.

The reason it matters now: a lot of people are sitting in a low-income window — early retirement, a career gap, the years before Social Security kicks in — and paying taxes at a rate they'll never see again. Every year they don't act is a year of cheap conversion capacity they can't get back.

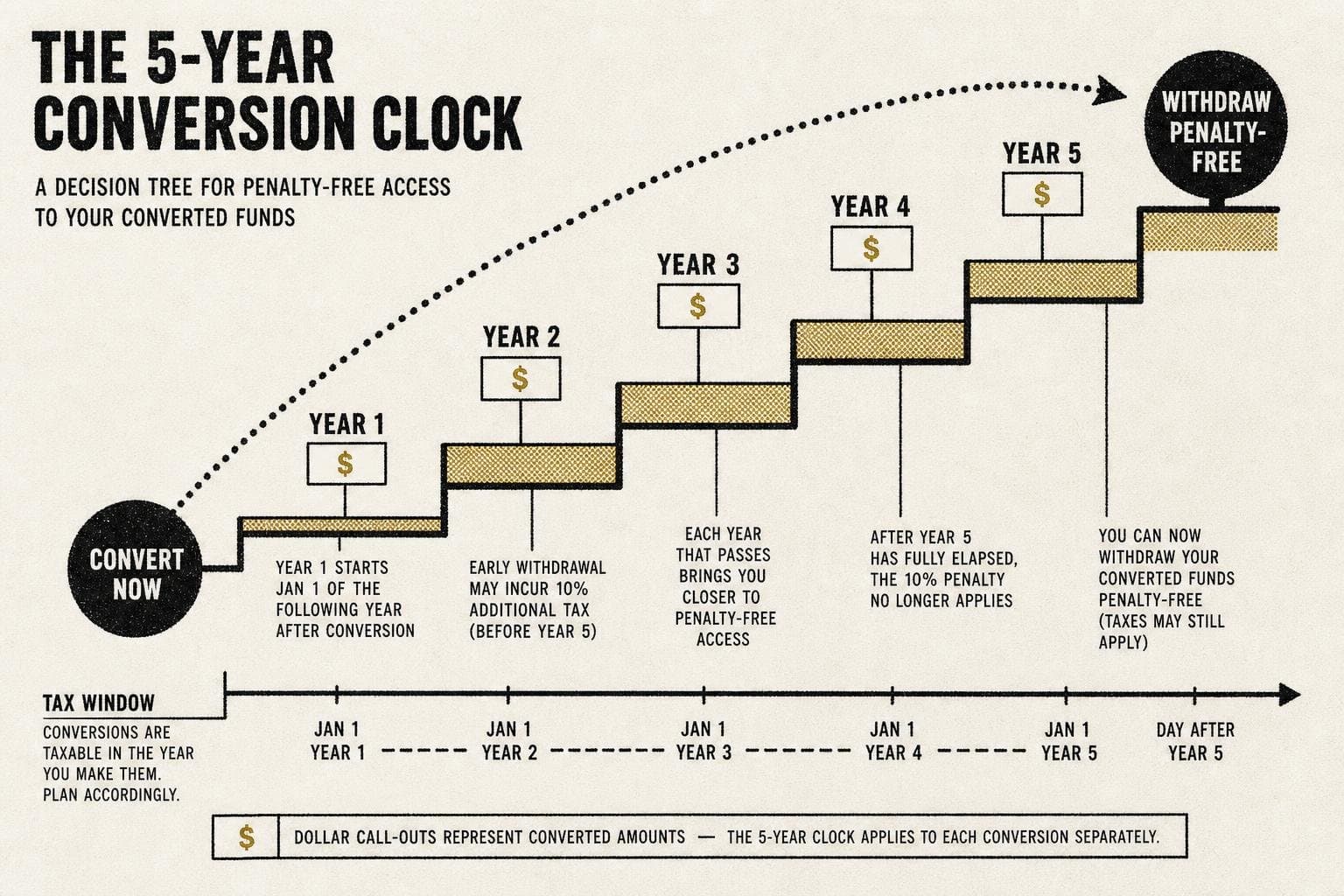

The Mechanics Are Simpler Than They Sound

Here's the core structure. You convert a chunk of your traditional IRA or 401(k) to a Roth IRA. You pay ordinary income tax on that amount in the year you convert. Then you wait five years. After five years, that converted principal — not the earnings, just the principal — is available to withdraw penalty-free, even if you're under 59½. Each conversion gets its own five-year clock, starting January 1 of the conversion year.

As Money&Planet explains, a conversion done in December 2026 is treated as if it happened January 1, 2026 — meaning the principal becomes accessible January 1, 2031. That calendar quirk is worth knowing: a late-year conversion gets you nearly a full year of clock for free.

The strategy is built for a specific person: someone who plans to stop working at least five years before 59½ and has a meaningful pre-tax balance to convert. If you're still in peak earning years and your income is high, the math usually doesn't work — you'd be converting at a rate higher than you'd pay in retirement. The ladder only makes sense when your current tax rate is lower than your expected future rate.

The Tax Window Is the Whole Point

The reason this works is that federal tax brackets are progressive, and early retirement often creates a rare low-income stretch. Money&Planet notes that for a married couple filing jointly in 2026, the 12% bracket runs up to $100,800 of taxable income, per IRS 2026 inflation adjustments. Add the standard deduction for joint filers and you can convert a substantial amount annually without crossing into the 22% bracket — though the exact numbers depend on your full income picture and filing status.

The window gets even more valuable before Social Security starts. 247 Wall St. describes what planners call the "tax torpedo": once you turn on Social Security, every dollar pulled from a traditional IRA does double damage — it gets taxed at your ordinary rate and it drags more of your Social Security benefit into the taxable column. Roth withdrawals don't enter that formula. Converting before benefits start defuses the torpedo at the cheapest possible price.

This isn't just an early-retiree play. The Los Angeles Times recently covered a reader in her early 70s still working, whose husband is already taking required minimum distributions. The case for conversion there: shrinking the traditional IRA now lowers future RMDs, and any money converted can be inherited by kids tax-free — effectively paying their tax bill at a lower rate than they'd face in their peak earning years.

Where People Actually Get Burned

Two failure modes are common.

The first is the cash flow problem. You need money to live on during the five-year seasoning period before your first converted dollars are accessible. If you drain your bridge account — taxable savings, cash — before year five, you're stuck either taking early withdrawals with the 10% penalty or stopping the ladder mid-build. Money&Planet is direct about this: done badly, the ladder "runs your bridge account dry before the first conversion is even withdrawable."

The second failure mode is converting too aggressively and bumping into higher brackets, Medicare IRMAA surcharges, or increased Social Security taxation. Economist Laurence Kotlikoff has argued that the standard "fill up your bracket" advice is often wrong — optimal conversion amounts are a nonlinear problem that depends on Social Security timing, RMD projections, state taxes, and Medicare costs simultaneously. The bracket-filling heuristic is a starting point, not an answer.

One practical note: Charles Schwab flags that state tax treatment of Roth conversions varies — what's tax-free at the federal level may not be at the state level. Check your state's rules before assuming the math works the same way.

The Decision You're Actually Making

A Roth conversion ladder is a bet that your future tax rate will be higher than your current one. If you're right, you win. If tax rates fall dramatically or your retirement income ends up lower than expected, you overpaid. Nobody knows the future, but you can make a reasonable estimate based on your current income, your projected RMDs, and when you plan to claim Social Security.

The question worth sitting with: what's the cost of doing nothing? For most people in a genuine low-income window, it's paying a higher rate on the same dollars later — plus losing the compounding that would have happened inside a Roth. That's not a hypothetical. It's a number you can actually calculate.