The standard rent-vs-buy calculator asks for your home price, your mortgage rate, and how long you plan to stay. It spits out a monthly number. You compare it to your rent. You make a decision.

The problem is that the calculator is only counting the mortgage. The rest of homeownership — the part that actually determines whether buying was a good decision — doesn't fit neatly into a form field.

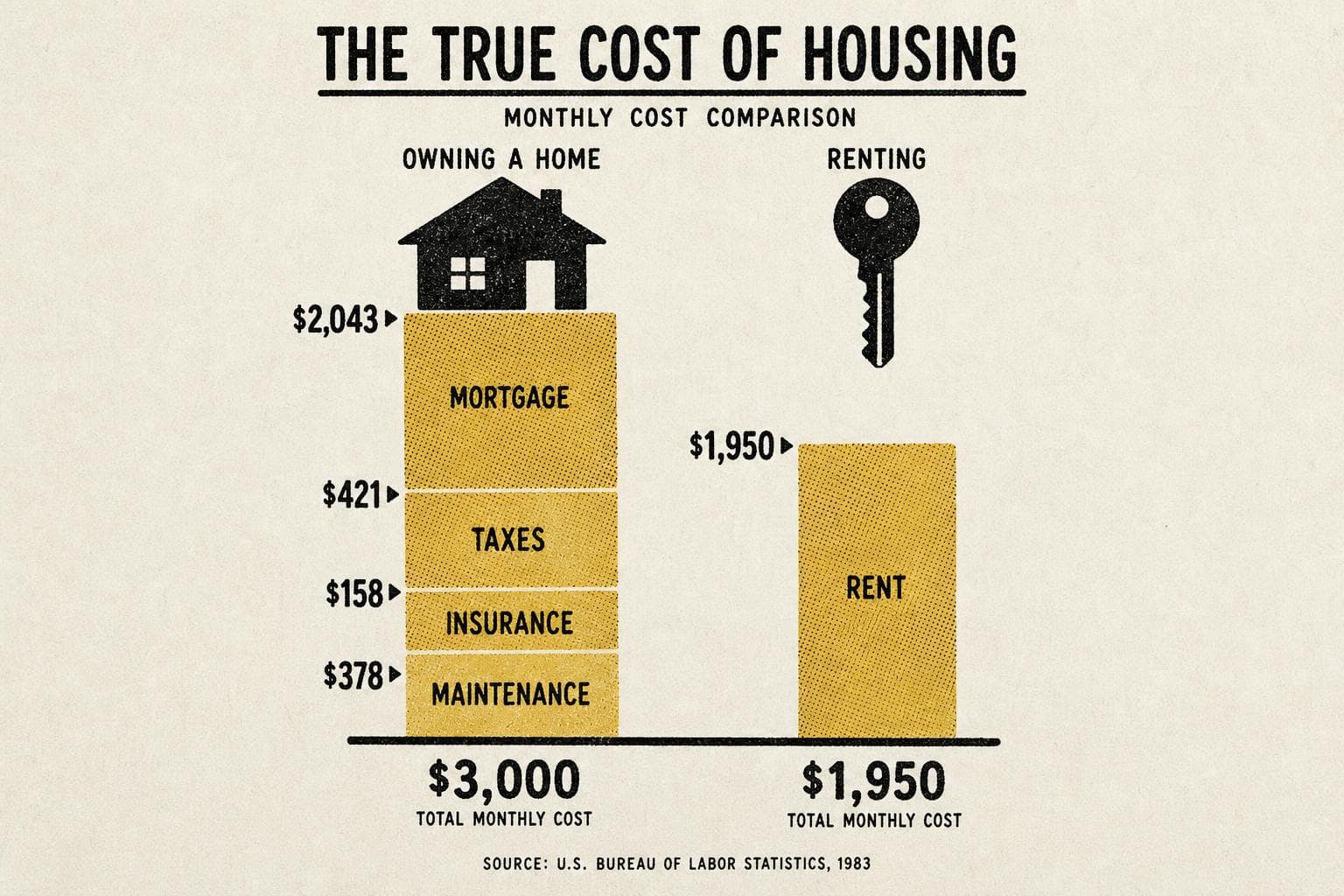

The $10,000 Line Item Nobody Mentions

Here's a number worth sitting with: in 2024, property taxes, homeowners insurance, and maintenance added an average of $10,535 per year for owners with a mortgage, according to BLS data via Motley Fool's analysis. That's roughly $878 a month on top of your mortgage payment — costs that renters largely avoid.

That same BLS data shows homeowners with a mortgage spent an average of $27,039 on housing and utilities in 2024, compared to $19,572 for renters. The mortgage-vs-rent gap looks manageable. The total-cost gap is nearly $7,500 a year.

None of that $10,535 builds equity. It just keeps the house standing and the county off your back.

The Closing Cost Ambush

Before you even make your first mortgage payment, there's another number the calculator skips: closing costs.

These run 2% to 5% of the purchase price and are separate from your down payment, according to a 2026 guide from AmeriSave. On a $400,000 home, that's $8,000 to $20,000 in cash you need at the table — for appraisals, title searches, lender processing, and government recording fees that don't add a dollar to your equity. The CFPB reported a 36% increase in median total loan costs between 2021 and 2023, per that same guide.

So the actual cash requirement on day one isn't just your down payment. It's your down payment plus closing costs plus whatever reserves your lender requires. Most calculators show you one of those three numbers.

The Costs That Don't Stay Flat

Property taxes and insurance aren't fixed. They adjust — usually upward — and they're not optional. The Washington Post reported in April that buyers tend to focus on purchase price and mortgage rate while ignoring these two "nonnegotiable" parts of their housing payment. A study by Neighbors Bank found they represent a significant share of total monthly costs, though the exact figures vary by market.

This is where the rent-vs-buy framing breaks down. Rent has one number. Ownership has a mortgage (which can be fixed), plus property taxes (which reset with reassessments), plus insurance (which has been rising sharply in many markets), plus maintenance (which is unpredictable by definition). You're not comparing one monthly payment to another. You're comparing a fixed cost to a portfolio of costs with different volatility profiles.

I'd argue this is the actual source of homeownership financial stress for most people — not the mortgage payment they planned for, but the three other line items they didn't model.

Reality Check: "Building Equity" Isn't a Counterargument

The standard response to all of this is: yes, but you're building equity. True. Each mortgage payment does reduce principal, and home values can appreciate over time. The BLS data acknowledges this — ownership can carry a financial benefit not captured in annual spending comparisons for owners who stay long enough.

But equity is a long-term, illiquid, unrealized asset. Property taxes are a monthly cash obligation. Insurance is a monthly cash obligation. A failed water heater is a same-week cash obligation. These don't net against each other in your checking account. You can be equity-rich and cash-flow-stressed simultaneously, which is exactly the situation a lot of homeowners find themselves in and didn't anticipate when they ran the calculator.

The One Number to Add Before You Decide

Before you compare your potential mortgage payment to your current rent, add this to the mortgage side: an estimate of annual property taxes and insurance for that specific property (your county assessor's website and an insurance quote will get you close), divided by 12. Then add 1% of the home's value annually as a rough maintenance placeholder — not a rule, just a starting assumption you can adjust.

That revised monthly number is what you're actually comparing to rent. If it still works, great. If it doesn't, you haven't been talked out of buying — you've just found the real constraint to solve for.