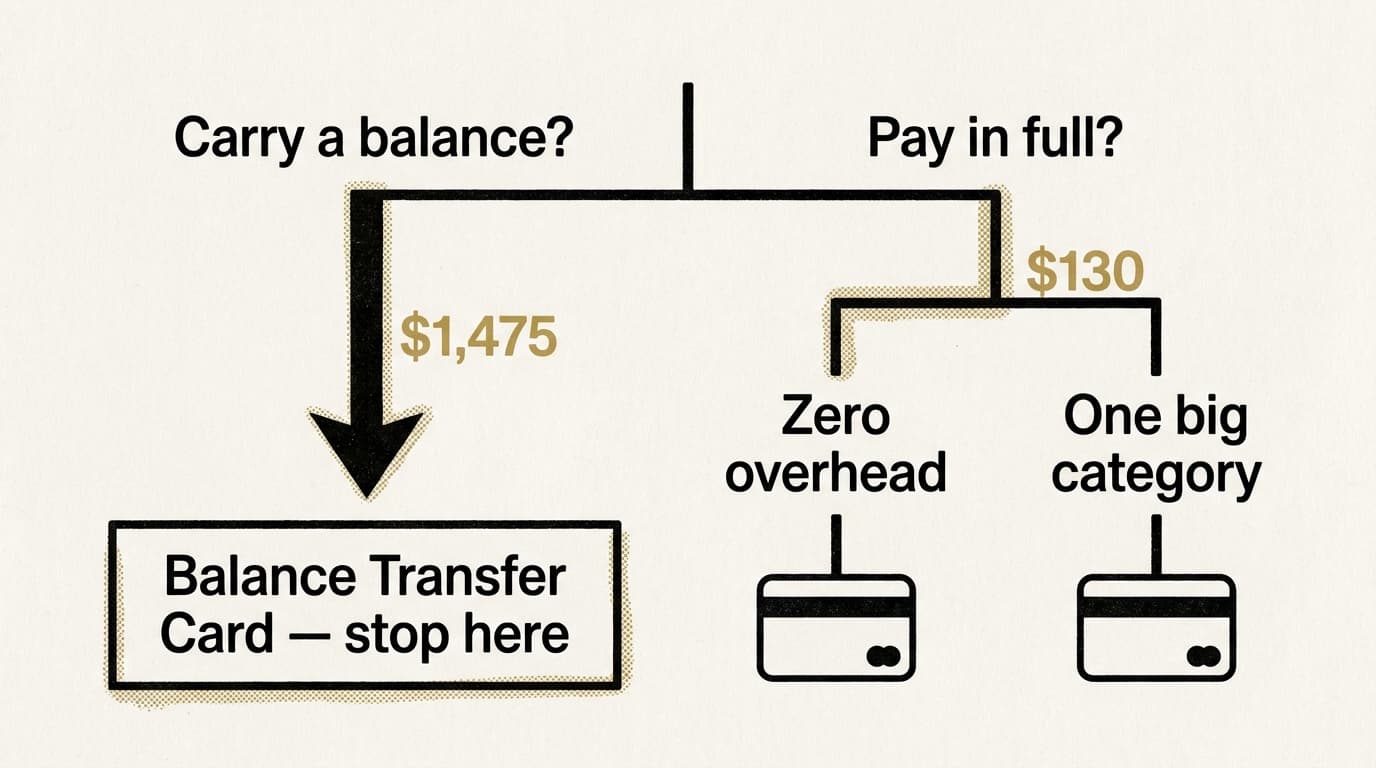

Here's the math that most rewards content skips: if you carry a $6,500 balance at a 23% APR, you're paying roughly $1,475 a year in interest. A 2% cash back card on average spending returns maybe $130. That's a net loss of around $1,345 annually — not a rewards strategy. It's a subscription to your own financial drain.

This is why "credit card optimization" advice is mostly useless for nearly half the people reading it. About 46% of American cardholders carry a balance month to month, and for them, the entire rewards conversation is noise. If that's you, the only optimization that matters is a 0% intro APR balance transfer card — full stop. Everything else is rearranging deck chairs.

But if you pay in full every month? You're who this is actually for.

The Complexity Trap Costs More Than the Rewards Are Worth

The points-optimization world has a seductive internal logic: stack the right cards, hit the right categories, transfer to the right airline partners, and you're flying business class for free. Some people genuinely do this well. They are not most people, and they are probably not you.

The behavioral pattern is consistent: people overestimate how much they'll spend in bonus categories and underestimate the mental overhead of managing multiple cards, annual fee calendars, and redemption windows. A card offering 5% on groceries and 3% on gas sounds better than flat 2% everywhere — until you realize you're mentally categorizing every purchase, occasionally missing a category, and paying an annual fee that requires a specific spending threshold just to break even.

I'd argue the optimization math almost always favors simplicity, because the "lost" rewards from a flat-rate card are smaller than they appear, while the friction costs of a complex setup are larger. Time spent tracking points is time not spent on things that compound better.

The Actual Decision Tree Is Short

For most people who pay their balance in full, the decision comes down to two questions:

Do you want zero mental overhead? Get a flat 2% cash back card with no annual fee. The Wells Fargo Active Cash has won NerdWallet's best simple cash back card designation every year from 2022 through 2026 for exactly this reason — 2% on everything, no categories, no annual fee, no math. You will never need to think about it again.

Do you have one dominant spending category that's genuinely large? Then a single category card layered on top of a flat-rate card can make sense — but only one, and only if the annual fee math works out clearly in your favor before you add any aspirational spending projections.

That's the whole tree. Two branches. The points-obsessive version has seventeen branches and requires a spreadsheet. The seventeen-branch version is how you end up with four cards, two of which you forgot you're paying annual fees on.

Reality Check: "Points Are Free Money" Is the Industry's Best Marketing Line

The rewards ecosystem is funded by merchant swipe fees (typically 1.5–3.5% per transaction) and, more significantly, by interest payments from the 46% of cardholders who carry balances. Card issuers call full-payers "transactors" — the people they actually lose money on. Your cash back isn't a gift. It's a cross-subsidy, and the industry is fine with you believing it's magic because that belief keeps you engaged with a product that occasionally converts transactors into revolvers.

None of this means you shouldn't take the cash back. You absolutely should. But treating rewards as the primary variable in a card decision — rather than fee structure, interest rate, and your own actual spending patterns — is exactly what the industry wants you to do. It keeps the conversation on their terms.

The Next Step Is Boring, Which Means It's Probably Right

Pull up whatever card you're currently using. Check the annual fee. Check whether you've actually redeemed anything in the last 12 months. If you're paying a fee and not redeeming, you're not optimizing — you're just paying a fee.

If you're carrying a balance, the only move is a balance transfer to a 0% intro APR card and a plan to pay it down before the promotional period ends. Rewards can wait.

If you're paying in full and your current card is a flat 1.5% or better with no annual fee, you're probably already done. The marginal gain from switching is smaller than the time it takes to evaluate switching. Close the seventeen-tab browser session and go do something else.

The best credit card setup is the one you never have to think about. That's not a compromise. That's the point.