Most people pick their health insurance by looking at one number: the monthly premium. The lower it is, the better the deal. This is exactly backwards.

The premium is what you pay whether you use healthcare or not. The deductible is what you pay when you actually need it. Optimizing for the first number while ignoring the second is like choosing a car based on the sticker price without checking what gas costs.

And yet — 30% of employer-insured workers were on high-deductible plans by 2023, up from 4% in 2006. A lot of that growth wasn't driven by people making careful tradeoff calculations. It was driven by sticker shock at the premium line.

The Actual Math You Need to Do

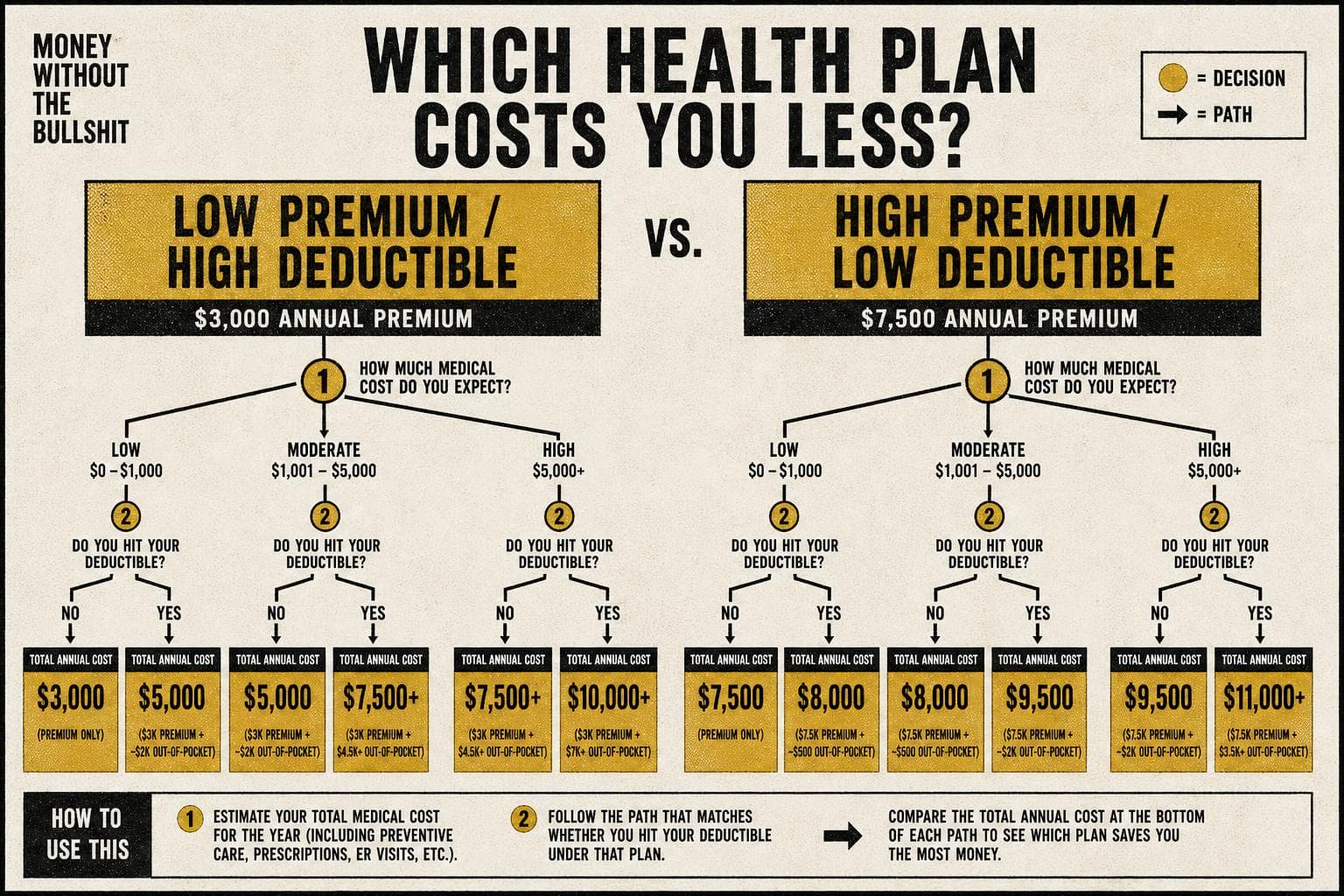

Here's the decision framework most people skip: compare total annual cost, not monthly cost.

Take your premium and multiply it by 12. That's your floor — what you pay even if you never see a doctor. Then add your expected out-of-pocket costs based on how much care you actually use. That number is what you're comparing between plans.

A lower-premium, high-deductible plan often wins if you're young, healthy, and rarely need care. It can lose badly if you have a chronic condition, a family with kids, or a year where something goes wrong. The teacher profiled by KFF Health News learned this the hard way: she picked the cheapest plan on the exchange without realizing her husband's coverage wouldn't kick in until they'd paid thousands out of pocket first. "I didn't know what a deductible was, so I just went with what was cheap, and now I have regret," she said.

That's not a financial literacy failure. That's a system designed to obscure the real cost until you're already in it.

The HSA Offset Most People Leave on the Table

Here's where the strategy actually gets interesting — and where most people leave real money behind.

If you're enrolled in a qualifying high-deductible plan, you're eligible for a Health Savings Account. The triple tax advantage is real: contributions reduce your taxable income, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. Charles Schwab notes that for 2026, individual contribution limits are $4,400 ($8,750 for families), with an additional $1,000 catch-up if you're 55 or older.

The catch: most people use their HSA like a checking account, spending it down every year on copays and prescriptions. That's fine, but it misses the bigger play. If you can afford to pay current medical expenses out of pocket and let the HSA balance grow invested, you're building a tax-free reserve specifically for healthcare costs — which tend to be highest in retirement, when you need it most.

The HSA only makes sense as an investment vehicle if you have the cash flow to cover your deductible without touching it. If a $5,000 deductible would wipe out your emergency fund, the high-deductible plan isn't a tax optimization strategy — it's a financial risk you're not pricing correctly.

The Unintended Consequence Nobody Talks About

High-deductible plans were designed on the theory that financial skin in the game makes people better healthcare consumers. Holmes Murphy's benefits analysts push back on this: people don't make healthcare decisions the way economists assume. When faced with a high deductible, many people delay or skip care — not because they're being prudent, but because the cost is scary and the system is confusing. Preventive care gets skipped. Small problems become bigger ones.

The rational-consumer model works fine for buying a TV. It works less well when you're deciding whether to take your kid to urgent care at 11pm.

Reality Check: "HDHPs are only for healthy young people."

Not quite. They can work well for people with predictable, manageable healthcare needs — regardless of age — when paired with a funded HSA and a real cash cushion. The plan type isn't the problem. The problem is choosing it based on the premium alone, without modeling what happens when you actually use it.

The next step: Pull up last year's Explanation of Benefits statements and add up what you actually paid out of pocket. Then compare that number — not just the premium — against what you'd pay under a different plan. If you've never done this math, you're probably on the wrong plan.