Mortgage rates have dropped below 6% for the first time in over three years, according to Yahoo Finance. Your inbox is probably already full of lender emails. Here's the one number that actually matters before you respond to any of them.

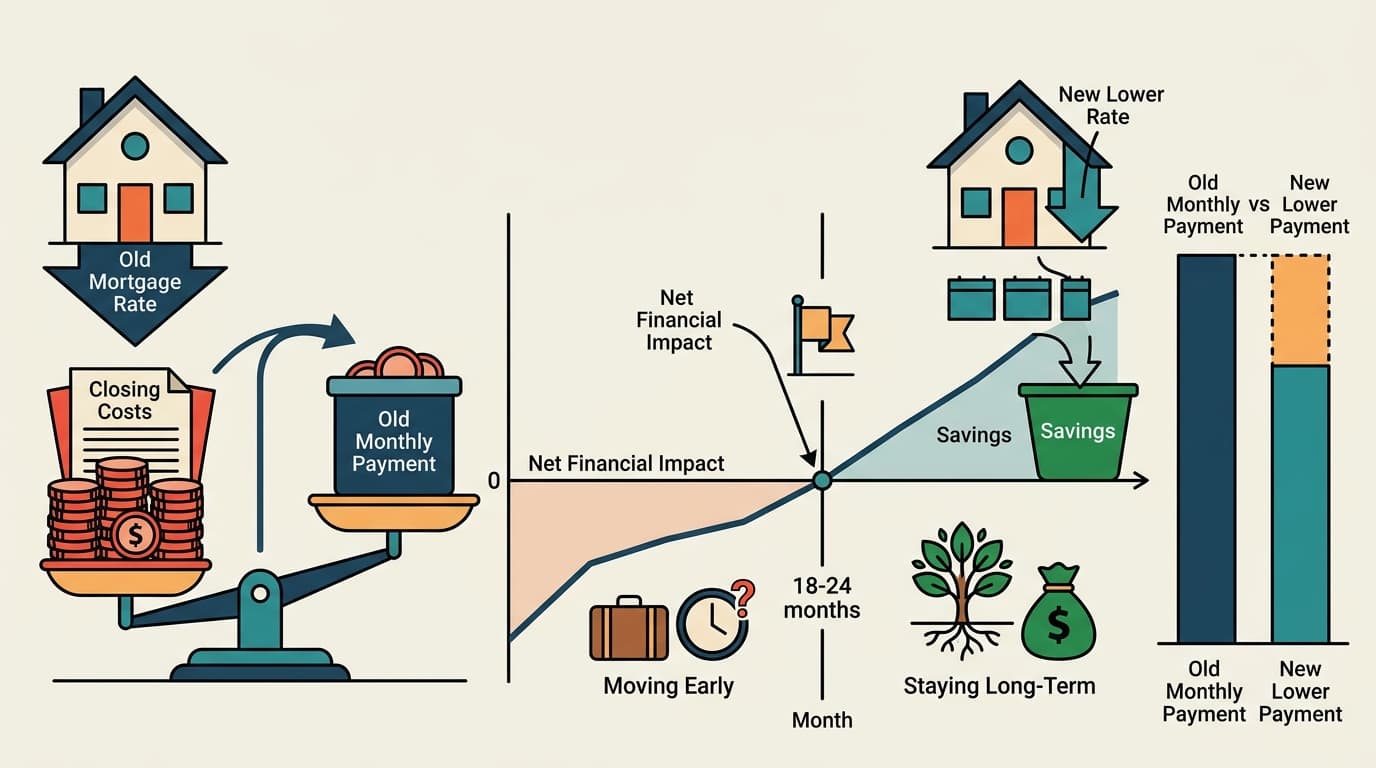

Closing costs divided by monthly savings. That's your break-even point — the month when refinancing stops costing you money and starts saving it. Melissa Cohn, regional vice president at William Raveis Mortgage, puts the target at 18 to 24 months. If you're not going to hit that threshold, you're not refinancing — you're just doing paperwork and paying fees.

The math is unforgiving on small rate drops. The Mortgage Reports estimates that dropping from 7% to 6.5% on a $400,000 loan saves roughly $133 a month — which sounds good until you realize typical closing costs run several thousand dollars. At that savings rate, you're looking at close to five years just to break even. Move before then and you've lost money on the transaction.

The conventional wisdom — "refinance when you can drop 1-2%" — exists for a reason, but it's a shortcut, not a rule. A 1% drop might pencil out in 18 months or 48 months depending on your loan balance, your closing costs, and how long you're staying. The percentage is a starting filter. The break-even calculation is the actual answer.

Reality Check: "Refinancing resets your loan and costs you equity."

True, but usually irrelevant. Yes, refinancing into a new 30-year term means you're paying more interest over the full life of the loan — if you stay for 30 years. Most people don't. If you're planning to sell in seven years and your break-even is 20 months, the equity math is a distraction. Run the numbers for your actual timeline, not a theoretical one.

The specific next step: get a Loan Estimate from your current lender (they're required to provide one), find the closing costs line, divide by your projected monthly savings, and compare that number to how many months you realistically plan to stay in the house. If the break-even lands inside that window with room to spare, refinancing makes sense. If it doesn't, the rate drop isn't for you — yet.