The standard advice sounds so clean: save six months of expenses, done. But "six months" is a number that was designed for a person who doesn't exist — stable W-2 income, two earners, no chronic health issues, predictable expenses. If that's not you, the rule isn't wrong exactly. It's just aimed at someone else.

The more useful question isn't how many months but which months — and whether the number you're targeting actually matches the risk you're actually carrying.

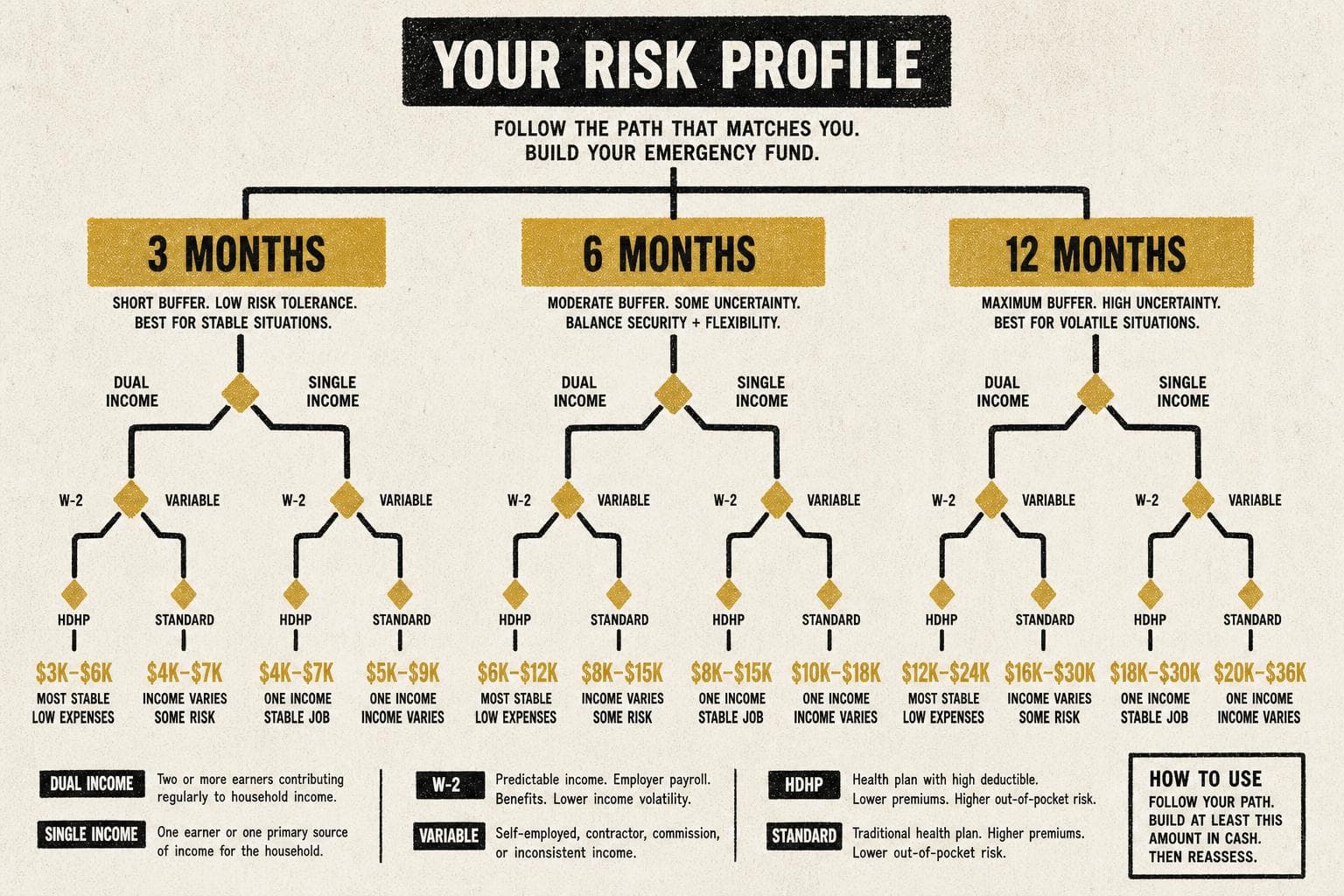

Your Emergency Fund Is Sized for a Specific Failure Mode

Think of an emergency fund as insurance against a specific scenario: income stops, expenses don't. The fund buys you time to fix it.

That framing immediately reveals why the generic rule breaks down. The time you need depends on how long it takes to replace your income — and that varies enormously by how you earn it.

A W-2 employee with a working spouse and a marketable skill in a stable industry has a very different re-employment timeline than a freelance contractor, a commission-based salesperson, or a single-income household with kids. According to Numeraty's April 2026 analysis, the Bureau of Labor Statistics data shows that median unemployment duration for self-employed workers runs longer than for wage employees during recessions — which is exactly when you're most likely to need the fund.

The rule of thumb doesn't adjust for any of this. You have to.

The Variable You're Probably Ignoring

Most people calculate their emergency fund target off their spending, which is the right instinct. But there's a second variable that almost nobody accounts for: the likelihood and cost of the emergency itself.

Two examples where the standard math fails:

High-deductible health plans. If you're on an HDHP, your out-of-pocket maximum for 2026 is $8,300 for individuals. A serious medical event doesn't just threaten your income — it creates an immediate cash demand. Your emergency fund needs to absorb both simultaneously. Six months of rent money doesn't help if you're also carrying $8,000 in medical bills on a credit card at 20%+ APR.

Variable income. If a meaningful chunk of your compensation comes from bonuses, RSUs, or commissions, calculating your fund off total comp overshoots; calculating it off base salary undershoots. Woven Capital's framework for variable-comp earners makes the logic explicit: in an actual emergency, the variable income disappears first. Your fund needs to cover the lifestyle you've built, not just the salary that anchors it — but sized against what you'd actually live on if the variable income stopped cold.

Reality Check: "3 Months Is Fine If You Have Job Security"

This one sounds reasonable and is mostly wrong. "Job security" is not a property of your job — it's a probability estimate you're making about the future, usually based on how stable things feel right now. The people who felt most secure in 2008 were often the ones least prepared.

The more honest version: 3 months may be fine if you have dual income, low fixed expenses, no dependents, and a skill set with fast re-employment timelines. That's a specific profile, not a general reassurance. If you're checking all four boxes, 3 months is a defensible floor. If you're checking two of them, it's probably not.

The Federal Reserve's 2024 SHED data found that 37% of adults couldn't cover a $400 emergency with cash — a number that has barely moved in three years. The people most likely to be in that 37% are also the people most likely to have been told that 3 months is "fine."

The Actual Next Step

Run this quick triage before you decide whether your current fund is right-sized:

- Single or dual income? Single income with dependents: add 2-3 months to whatever target you had.

- W-2 or variable/self-employed? Variable or self-employed: your floor is 9 months, not 6.

- High-deductible health plan? Add your out-of-pocket maximum as a separate line item — not folded into monthly expenses.

- How long would re-employment realistically take? Be honest. Not "how long did it take last time" but "how long in a bad economy."

If the number you land on is bigger than what you have, that's not a reason to panic — it's a reason to have a specific target instead of a vague aspiration. The fund you're building is sized for your actual risk profile, not a hypothetical median household that may not look anything like yours.