The standard emergency fund advice has survived for decades because it's directionally correct: having a cash buffer is better than not having one. But "3-6 months of expenses" is a range so wide it's almost meaningless. Three months is 50% less than six months. For most households, that gap is tens of thousands of dollars. The rule doesn't tell you where in that range you belong — and that's the only part that actually matters.

The math isn't complicated. Most people just haven't done it for their specific situation.

You're Probably Calculating the Wrong Number

Here's the first mistake: most people calculate their emergency fund target based on total monthly spending, not essential monthly expenses. Those are different numbers.

Your total monthly spending includes dinners out, streaming subscriptions, gym memberships, and the occasional impulse purchase. None of that needs to be covered by an emergency fund. An emergency fund exists to bridge you through a crisis — a job loss, a medical event, a major unexpected expense — without forcing you to take on high-interest debt or liquidate investments at the wrong time. As finbarrow's analysis of emergency fund math puts it, the expenses an emergency fund is genuinely for share three features: they are unplanned, unavoidable, and would otherwise force a financially destructive response.

So the base calculation is: what are your essential monthly expenses? Rent or mortgage, utilities, groceries, insurance, minimum debt payments, transportation to work. For most households, that number is meaningfully lower than total spending. If your total monthly outflow is $6,000 but your essential floor is $3,800, you're sizing your fund against the wrong denominator — and either over-saving cash that could be invested, or under-saving because the full number felt unreachable.

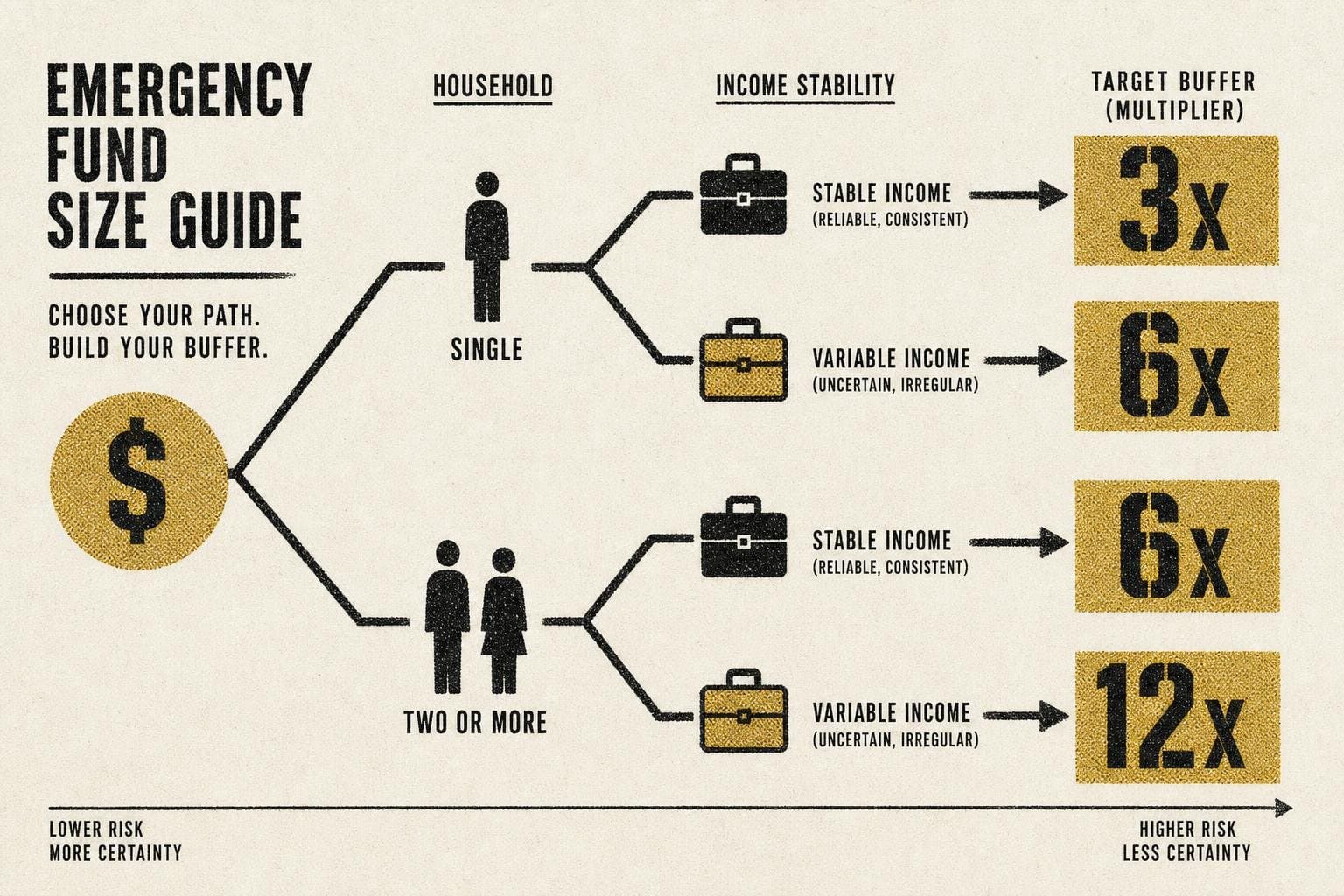

Your Risk Profile Sets the Multiplier

Once you have the right base number, the 3-6 month range is actually a risk-adjustment variable, not a suggestion to split the difference.

Aedilis's breakdown of emergency fund sizing lays out the logic cleanly: three months of essential expenses may be appropriate if you have a stable W2 job, work in an industry with strong job mobility, and have another income earner in your household. Six months or more is the right target if you're self-employed, work on commission, have significant fixed expenses that can't be cut, or are the sole earner supporting dependents.

The variable the rule never mentions is job search duration. Three months feels like real protection until you look at how long displaced workers actually spend job hunting — and that number varies significantly by industry, seniority level, and economic conditions. 247 Wall St.'s coverage of the 1-3-6 method makes this point directly: three months of expenses "protects you against most things except for job loss" — which is, for most people, the scenario the fund is actually for.

Two households at identical income levels can arrive at very different correct answers. A dual-income household where both partners work in stable industries with low unemployment might be fine at three months of essential expenses. A single-income household where the earner is a freelance contractor in a cyclical industry should probably be at nine to twelve months — and should be calculating against essential expenses only, or the target becomes paralyzing.

The Opportunity Cost Problem Cuts Both Ways

There's a version of this conversation that goes: "your emergency fund is too small, you're one bad month from disaster." There's another version that goes: "your emergency fund is too large, you're leaving money on the table." Both are real failure modes.

The Federal Reserve's 2025 Economic Well-Being report found that financial fragility — the inability to cover unexpected expenses — remains a persistent problem across American households. That's the under-saved failure. But the over-saved failure is quieter and more common among people who are otherwise financially functional: cash sitting in savings beyond what your actual risk profile requires is cash that isn't compounding. The americandefault.org summary of buffer depletion data notes the personal savings rate has fallen to roughly 4%, which suggests most people aren't in danger of over-saving — but if you've already built a substantial fund and haven't revisited the math since your circumstances changed, it's worth checking.

The right emergency fund size isn't a fixed number. It's a function of your essential expense floor, your income stability, your household structure, and your realistic job search timeline if things go sideways. Run those numbers once. You'll end up with a specific target instead of a range — and a specific target is something you can actually work toward.

If you want to go deeper on the health insurance side of emergency planning — specifically how your deductible interacts with your cash buffer — the April issue on deductible math covers that tradeoff directly.