The most common piece of refinancing advice is that you should refinance when rates drop at least 1% below your current rate. It's tidy, memorable, and wrong — or at least, wildly incomplete. Whether a refinance makes financial sense has almost nothing to do with the rate gap and almost everything to do with how long you plan to stay in the house.

Here's the actual math.

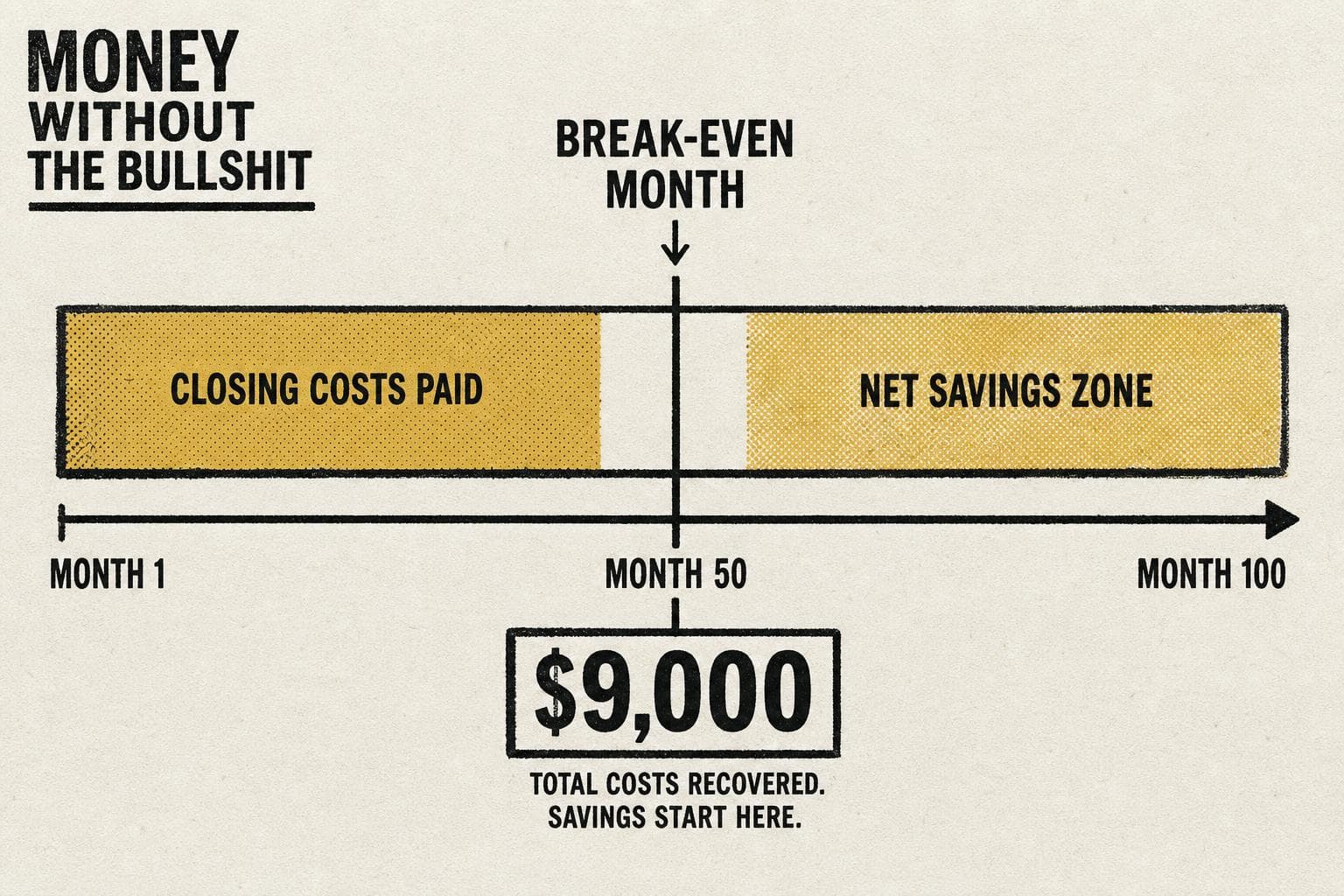

The Only Number That Actually Matters: Your Break-Even Point

Refinancing isn't free. Closing costs typically run 2–5% of the loan balance — on a $350,000 mortgage, that's $7,000 to $17,500 out of pocket (or rolled into the new loan, which has its own cost). That money is gone before you save a single dollar on your monthly payment.

The break-even point is when your cumulative monthly savings finally exceed those upfront costs. NerdWallet's breakdown of the calculation makes the structure clear: add up all closing costs, divide by your monthly savings, and that's how many months until you're actually ahead.

Example: You refinance a $300,000 balance and pay $9,000 in closing costs. Your new payment is $180/month lower. Break-even: 50 months — just over four years. If you sell or refinance again before then, you lost money on the transaction. The rate drop doesn't matter. The timeline does.

This is why the 1% rule fails. A 1% rate reduction on a $150,000 remaining balance with $8,000 in closing costs might take six or seven years to break even. The same rate reduction on a $600,000 balance with identical closing costs might break even in 18 months. Same rate gap, completely different decision.

The Variables the Rate Comparison Ignores

How much loan you have left. Monthly savings scale with balance. A smaller remaining balance means smaller absolute savings per month, which means a longer break-even. If you're 20 years into a 30-year mortgage, refinancing into a new 30-year loan also resets your amortization clock — you'll be paying mostly interest again at the start, which extends the real cost.

Whether you're resetting the term. Refinancing from a 30-year into another 30-year when you have 18 years left isn't just a rate decision — it's adding 12 years of payments. The monthly payment might drop, but the total interest paid over the life of the loan could increase even at a lower rate. A shorter-term refinance (say, into a 15-year) often costs more per month but saves substantially on total interest. These are different decisions with different math, and conflating them is how people end up feeling like they "saved money" while actually paying more.

What you do with the closing costs. Rolling closing costs into the loan is common and convenient. It's also a way to obscure the real cost — you're now paying interest on those costs for the life of the loan. On a $9,000 closing cost rolled into a 30-year loan, the actual cost is meaningfully higher than $9,000. Not catastrophically so, but enough to shift your break-even calculation.

Reality Check: "Rates Are Dropping, So Now Is the Time"

Bankrate projects average 30-year rates around 6.1% for 2026, with a possible range of 5.7% to 6.5%. That's a real improvement from recent highs, and yes, if you locked in at 7.5% in 2023, the math on refinancing is starting to look interesting.

But "rates are dropping" is a market observation, not a personal finance decision. The refinancing industry has a structural incentive to get you to transact — lenders collect closing costs whether or not the refinance benefits you. The 1% rule exists partly because it's easy to communicate and partly because it generates volume. It is not a break-even calculation.

The actual question is: how long do you plan to stay in this house? If the answer is "probably five or six more years," run the break-even math before you do anything else. If the answer is "we're here until the kids finish high school," a refinance that breaks even in three years is a straightforward win. If the answer is "we're not sure," that uncertainty is the constraint — and locking in $10,000 in closing costs against an uncertain timeline is a bet, not a plan.

The next step is one calculation, not a rate comparison. Take your estimated closing costs (ask a lender for a loan estimate — it's free and they're required to provide one), divide by your projected monthly savings, and see how many months until you break even. Then ask yourself honestly whether you'll still be in the house by then. That answer tells you more than any rate forecast.