Most people treat refinancing like a weather event — something that happens to them when rates drop, not a decision with a calculable answer. That's how you end up doing a ton of paperwork to save $47 a month.

Here's the actual question: how long until the closing costs pay for themselves?

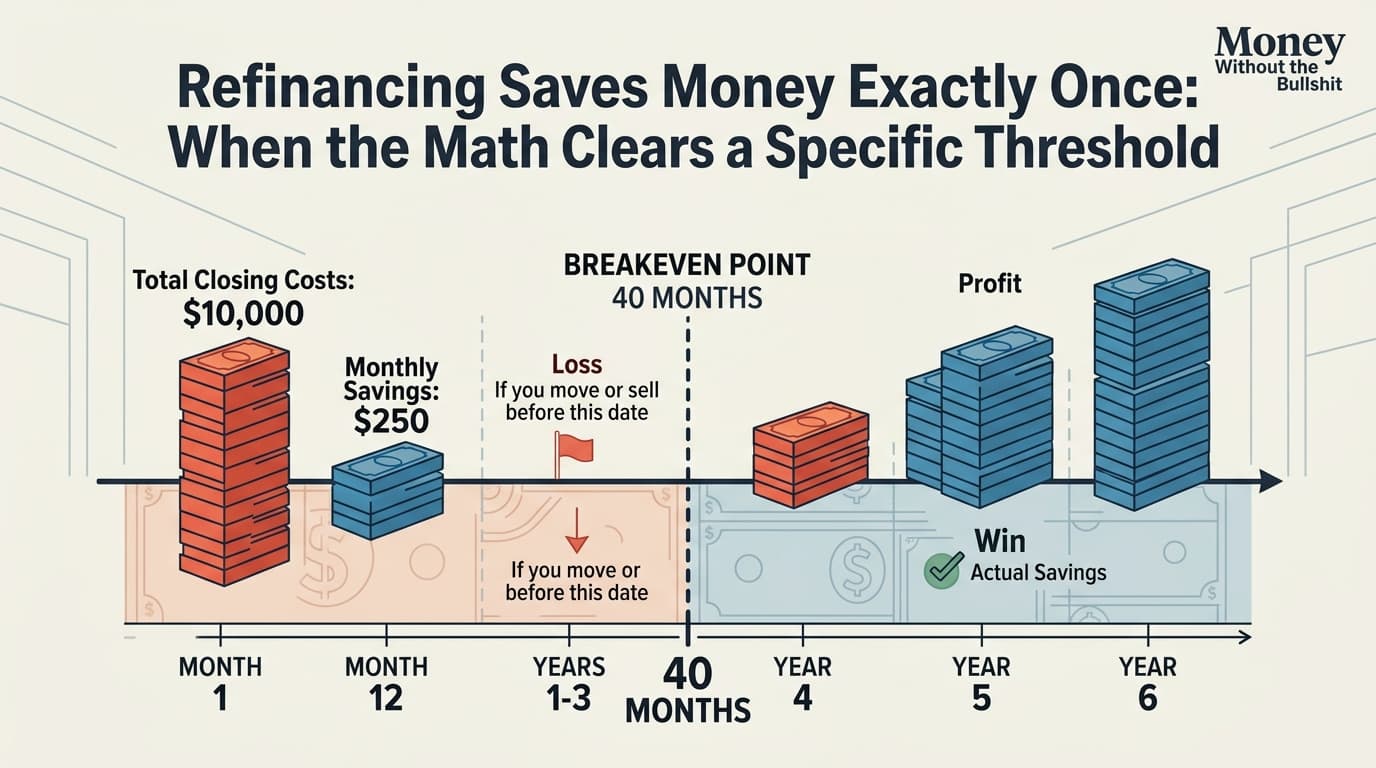

The Only Number That Matters

Refinancing costs money upfront. Closing costs typically run 2–5% of the loan amount — on a $300,000 balance, that's $6,000 to $15,000 out of pocket or rolled into the loan. Your monthly savings from a lower rate have to earn that back before you break even. If you're planning to sell or move before that date, you haven't saved anything. You've just paid for paperwork.

The break-even calculation is not complicated: divide total closing costs by monthly savings. If closing costs are $8,000 and you're saving $200/month, you break even in 40 months — about three and a half years. Stay longer than that, you win. Leave sooner, you lose.

Current 30-year fixed rates are sitting around 6.18%, up slightly from the prior week. That number matters because it sets your starting point for the savings calculation. If you locked in at 7.5% two years ago, the spread is meaningful. If you're at 6.5%, you're probably looking at a marginal monthly difference that takes years to recover.

When It Actually Makes Sense

Three situations where refinancing clears the bar:

You're dropping at least 1 full percentage point. This isn't a magic rule, but it's a useful filter. Smaller rate reductions produce smaller monthly savings, which means longer break-even timelines, which means more exposure to the risk that you move or rates drop further before you've recouped the cost.

You have enough runway. If you've been in your house five years and plan to stay another ten, a 36-month break-even is fine. If you're vaguely thinking about upsizing in two years, it's not.

You're not resetting the clock unnecessarily. Refinancing a 30-year mortgage you've been paying for eight years back into a new 30-year loan lowers your monthly payment but extends your total payoff date and increases lifetime interest paid. A 15-year refi often makes more sense if you can handle the higher payment — and 15-year rates are currently running lower than 30-year rates, which compounds the advantage.

When It's Just Paperwork

You're probably not saving money if:

- The rate difference is less than 0.75% and your loan balance is under $200,000 (the absolute dollar savings are too small to recover closing costs quickly)

- You're planning to move within three years

- You're rolling closing costs into the loan, which means you're paying interest on your closing costs for the life of the loan

- You're doing a cash-out refi primarily to fund consumption — you're not saving money, you're borrowing it against your house at mortgage rates, which are currently higher than they were two years ago

Reality Check: "Rates Have to Drop a Full Point Before It's Worth It"

This rule gets repeated constantly and it's not wrong, but it's incomplete. The 1% threshold is a heuristic for average loan sizes with average closing costs. On a $600,000 balance, a 0.6% rate drop might generate $250/month in savings and break even in under three years. On a $150,000 balance, a 1.5% drop might only save $100/month and take four years to recover. The percentage drop is an input, not the answer. The break-even timeline is the answer.

The Next Step

Pull up your current mortgage statement. Find your rate, remaining balance, and remaining term. Then get one actual rate quote — not a rate estimate, a real quote with a loan estimate form that shows closing costs. Plug those numbers into a break-even calculator (the CFPB has a free one). If break-even is under 36 months and you're confident you'll stay, it's probably worth doing. If it's over 48 months, it's probably not. Everything in between is a judgment call about your plans, not a math problem.

The decision takes about 20 minutes to evaluate correctly. Most people spend more time than that reading articles about whether rates might go lower next month — which is a question nobody can answer and that doesn't change the break-even math anyway.