There's a version of personal finance advice that treats all debt like a house fire. Get out fast, stop drop and roll, don't look back. And for high-interest revolving credit card debt, that instinct is basically correct — the math on minimum payments is genuinely brutal, with a $10,000 balance potentially generating $10,000–$15,000 in avoidable interest over the life of a minimum-payment-only payoff.

But the "pay everything off as fast as possible" rule breaks down the moment you apply it to all debt indiscriminately. The real question isn't how fast you can pay — it's what else you're giving up to do it.

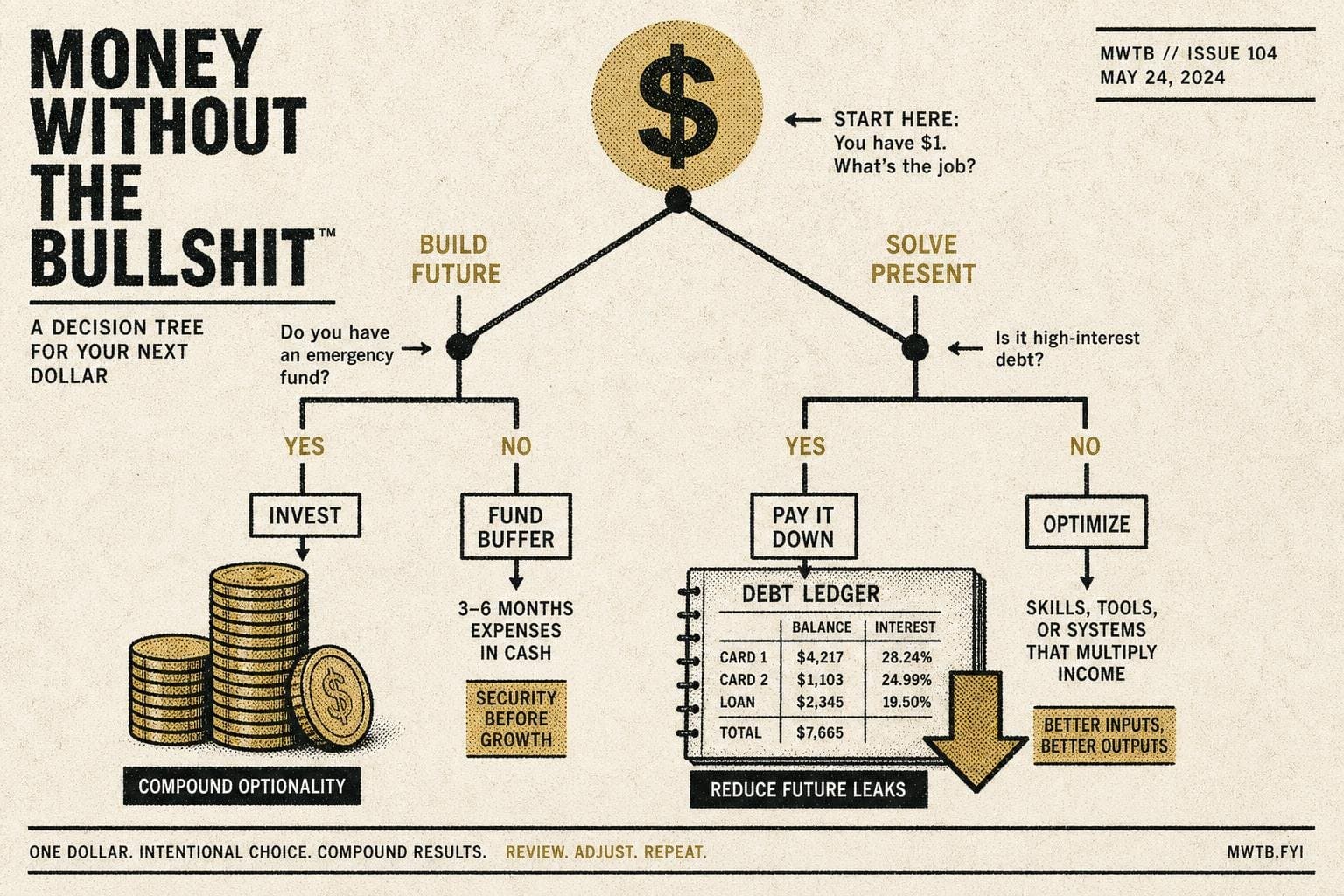

The Opportunity Cost Nobody Mentions

Throwing every spare dollar at debt feels productive. It's measurable, it's satisfying, and it's morally uncomplicated. The problem is that money is doing only one job when it could potentially be doing two.

The tradeoff looks like this: if your debt carries a relatively low fixed rate — think a federal student loan or a fixed-rate auto loan — and you have no emergency fund, no employer retirement match you're leaving on the table, and no high-interest debt elsewhere, then aggressive paydown of the low-rate debt might be the least efficient use of that cash.

This isn't a theoretical edge case. The Federal Reserve Bank of New York's most recent household debt report shows household debt balances rising slightly while delinquency transition rates hold steady — meaning a lot of people are carrying debt and managing it, not drowning in it. The "pay it all off immediately" advice is calibrated for crisis mode. A lot of people aren't in crisis mode. They're in optimization mode, and those require different decisions.

The constraint to identify first: what's the actual cost of not paying down this specific debt faster? That cost is the interest rate on the debt. Then ask: is there somewhere else this money earns more than that rate, or prevents a worse outcome?

When Minimum Payments Are a Reasonable Temporary Decision

The FTC's consumer debt guidance frames debt management as a triage problem — figure out what you owe, prioritize, negotiate where possible. That framing is more useful than the blanket "attack all debt" approach, because it forces you to rank.

Here's a rough decision tree for when slower paydown is defensible:

You have no emergency fund. Paying down a 6% student loan aggressively while carrying zero cash reserves means one car repair away from putting that emergency on a credit card at 20%+. You've traded a manageable low-rate debt for a high-rate one. The math on that trade is bad.

Your employer matches retirement contributions you're not maxing. An employer match is an immediate 50–100% return on that dollar, depending on the match structure. Almost no debt paydown strategy beats that return. Leaving the match on the table to pay off a 5% auto loan faster is a losing trade — though the exact calculus depends on your tax situation and match terms, which vary by employer.

The debt has a fixed rate and a defined end date. A structured installment loan — auto, student, personal — amortizes on a schedule. Unlike revolving credit card debt, which is engineered to keep balances revolving for years through minimum-payment formulas, an installment loan has a finish line. Paying it off two years early might save some interest, but it also depletes liquidity you might need.

None of this applies to high-rate revolving debt. Americans are currently carrying near-historic highs of credit card and auto loan debt, and the National Foundation for Credit Counseling is reporting a significant surge in people seeking credit counseling. For anyone in that category — carrying revolving balances at high rates — minimum payments are a trap, not a strategy.

The Actual Framework

Sort your debts by rate. Not by balance, not by emotional weight, by rate. High-rate revolving debt (credit cards, most personal loans) gets attacked aggressively — the interest math is unambiguous. Low-rate fixed debt (federal student loans at older fixed rates, some auto loans) gets paid on schedule while you redirect surplus cash to the emergency fund and any available employer match first.

The "pay off everything fast" rule is a useful heuristic for people who haven't thought about debt at all. But once you're past that stage — once you're functional but not optimized, which describes most people reading this — the better question is: what's the rate on this specific debt, and what's the best alternative use of the dollar I'd spend paying it down faster?

That's not a complicated calculation. It just requires treating debt paydown as a financial decision rather than a moral imperative.

The goal isn't to be debt-free as fast as possible. The goal is to be financially stable — and sometimes those aren't the same thing.