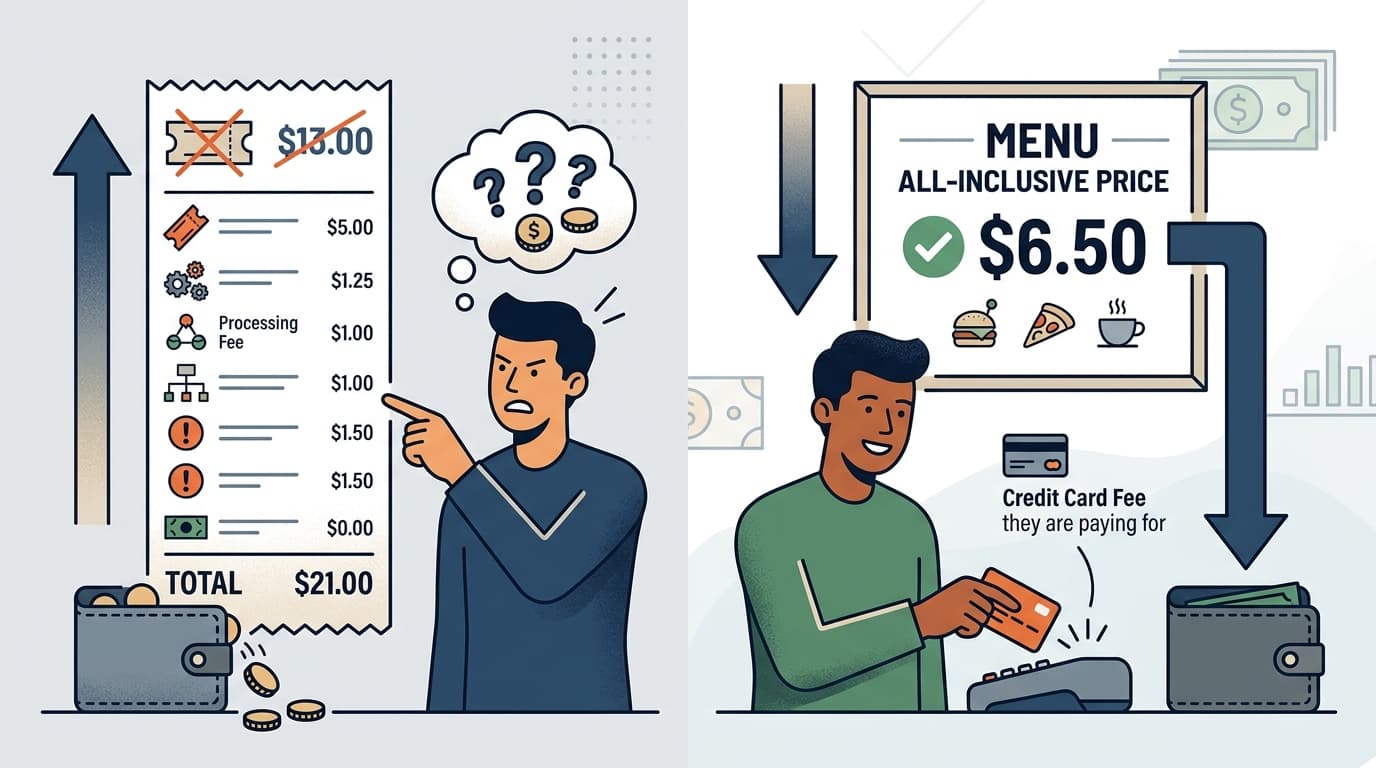

You're buying a $40 concert ticket. At checkout, there's a $6.50 "service fee," a $3.00 "facility charge," and a $2.50 "order processing fee." You pay $52. The ticket was never $40.

That's not a convenience fee. That's a pricing strategy that depends on you being too committed at checkout to walk away.

The distinction matters, because not all convenience fees work the same way — and treating them as a single category is how you end up either paying for everything or resenting fees that are actually worth it.

The Fee You're Paying Whether You See It or Not

Here's the uncomfortable part: in many cases, the cost exists regardless of whether it shows up as a line item. WSFS Bank notes that credit card surcharges — which can only be applied to credit transactions, not debit — are often a bundled recovery of processing fees, network fees, and security costs that businesses pay on every transaction. When a business absorbs those costs silently, they typically build them into base prices instead.

So the $3 credit card surcharge at your local coffee shop isn't necessarily extractive. It might just be honest pricing made visible. The alternative isn't free — it's hidden.

The genuinely predatory version is what the FTC moved against in May 2025: bait-and-switch fee structures where the advertised price bears no relationship to what you actually pay. That rule currently covers hotels, vacation rentals, and live-event ticket sellers — the industries with the most egregious track records. Everyone else is still operating in a gray zone.

The Fee That's Actually a Time Trade

Then there's the other category: fees you pay not because a business is hiding costs, but because you're buying back minutes you'd rather spend elsewhere.

Delivery fees, grocery pickup charges, same-day shipping — these are real costs with a real value proposition. The question isn't whether they're legitimate. It's whether the math works for you specifically.

A doxo report cited by ConsumerAffairs found Americans pay an average of $1,222 per household annually in hidden bill costs — a number that includes convenience-adjacent fees across utilities, subscriptions, and services. That's not a crisis. But it's also not nothing. Spread across a year, it's invisible. Looked at as a single number, it's a plane ticket.

The honest framework: if you're paying a convenience fee for time you genuinely value, that's a reasonable trade. If you're paying it because the checkout flow made opting out feel harder than just clicking through, that's a different thing entirely.

The Invisible Add-to-Cart Effect

The sneakiest version of convenience pricing isn't a fee at all. Retailers have shifted toward raising minimum spend thresholds to unlock "free" delivery rather than charging outright. The result: you log on to spend $30, add two items you didn't need to hit the free-shipping floor, and spend $55. No fee on the receipt. Technically you saved on shipping. Practically, you spent $25 more than you intended.

That's the fee that never shows up — and it's the one most worth watching.

Reality Check: "Just Use Cash to Avoid Surcharges"

Technically true. Practically, this advice ignores that cash has its own costs: ATM fees, the time to find an ATM, and the loss of purchase protections that come with credit cards. For most people, the better move is to use a debit card where surcharges don't apply, or to factor the surcharge into the real price before deciding whether to buy. Optimizing around a $2 fee by spending 20 minutes finding an ATM is not a win.

The next step is simple: for one month, flag every fee that appears at checkout that wasn't in the advertised price. Don't change your behavior yet — just notice. Most people are surprised by how often they're paying fees they never consciously agreed to, and how rarely they're paying ones that are actually worth it.