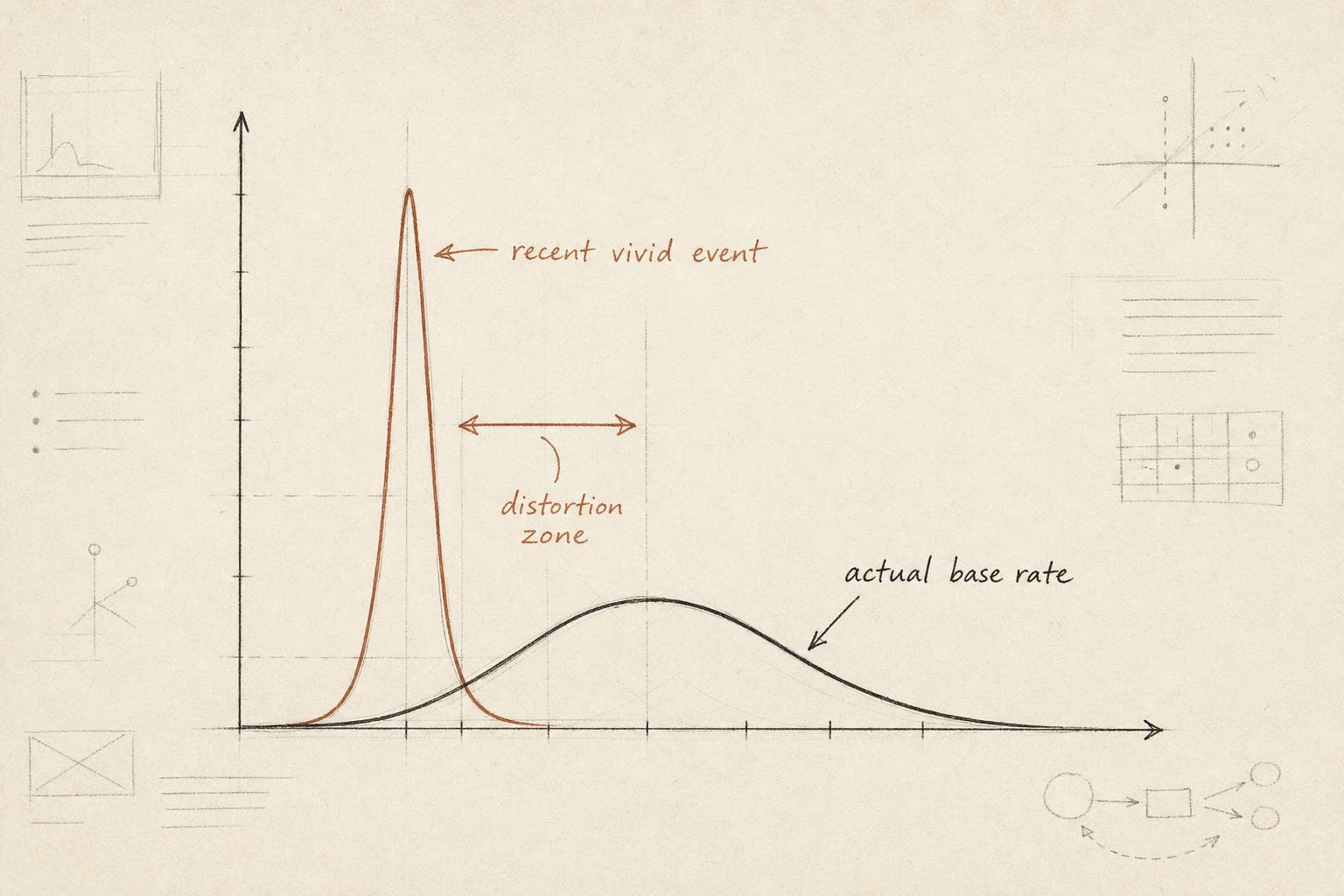

A single data breach story in the news can temporarily tank conversion rates across an entire industry. Not because the actual risk of fraud increased. Because the mental availability of fraud increased. As Atticus Li notes, as the news cycle moves on and the story fades, conversion rates typically recover — the underlying risk never changed, only how easily the example came to mind.

That's the availability heuristic in its purest form: we estimate the probability of something based on how easily we can recall an example of it. And "easily recalled" is heavily shaped by recency, vividness, and emotional charge — not by actual frequency.

The Bias Doesn't Disappear When You Add a Process

Here's the trap. Most organizations know about cognitive biases. They have risk frameworks, checklists, review committees. The assumption is that process neutralizes bias.

It doesn't. It just moves where the bias enters.

MIT Sloan's analysis of organizational resilience failures points to a consistent pattern across high-profile disasters — Southwest Airlines' holiday travel collapse, the Deepwater Horizon spill, the Norfolk Southern derailment: underlying problems were known and existed for a prolonged time, yet organizational responses lagged. The risks weren't invisible. They were boring. Chronic, slow-moving, not vivid. The availability heuristic doesn't just affect what we fear — it affects what we bother to monitor.

Recent, dramatic failures get intense scrutiny. The quiet systemic risks that haven't produced a crisis yet? They stay in the background, underfunded and under-examined, right up until they aren't.

When a Peer's Crisis Becomes Your Distortion

The availability effect gets stranger when you factor in what happens to organizations watching someone else fail.

Harvard Business Review research on reputational spillover shows that when a peer company experiences a crisis — a product safety failure, a regulatory violation, a scandal — customers, investors, and regulators often assume similar weaknesses exist across the industry. The peer's crisis makes the category of failure more mentally available, and that availability gets projected onto everyone nearby.

For risk managers, this creates a specific trap: the pressure to respond to the visible crisis in your industry, even when your actual exposure is different. Resources flow toward the risk that's in the news. The risk that's quietly building in your own operations — the one that doesn't have a recent vivid example — keeps getting deferred.

This is availability heuristic operating at the institutional level. The organization isn't asking "what are we actually most exposed to?" It's asking "what failure is most imaginable right now?" Those are different questions, and they produce different answers.

The Investment Version Is Just as Dangerous

Research on behavioral finance and investor psychology documents the same dynamic in markets: during crisis scenarios, investors systematically overweight the risks that are most cognitively available — the ones generating headlines — while underweighting risks that are structurally present but not recently dramatized. The result is amplified volatility and mispricing that can't be explained by the underlying fundamentals.

A bibliometric analysis of behavioral finance research across emerging economies found that one-sided availability-driven judgment directly affects risk tolerance assessments — investors systematically miscalibrate their exposure based on what's recently salient rather than what's statistically present.

The pattern is consistent whether you're an individual investor, a product team, or a risk committee: recent events don't just inform your probability estimates. They replace them.

The Practical Fix Is Boring on Purpose

The antidote isn't to stop paying attention to recent events. It's to build a deliberate counterweight: a process that forces attention onto the risks that haven't recently produced a vivid example.

Concretely, that means asking a different question in risk reviews. Not "what are we worried about right now?" but "what risks have we not discussed in the last six months, and why not?" The absence of recent examples is not evidence of low probability. It might just mean the risk is quiet — which is exactly when it's most dangerous to ignore.

Psyforu's synthesis of availability heuristic research frames it well: vivid, recent events disproportionately influence decision-making even when statistical evidence suggests otherwise. The bias operates unconsciously, affecting choices we believe are completely rational.

That last part is the one worth sitting with. The risk manager who just watched a competitor's supply chain collapse isn't feeling biased. They're feeling appropriately vigilant. The bias is invisible from the inside.

Try This: Pull up your organization's last risk review. Count how many items on the list were added in the past 90 days following a visible industry event. Then ask: what's been on the list for over a year without escalation? That second category is where the availability heuristic is probably doing the most damage.