Most of the coverage of the BLS Q1 2026 Productivity and Costs release led with the headline productivity figure. Reasonable choice. But buried three paragraphs in is a number that should have been the lede.

54.1%.

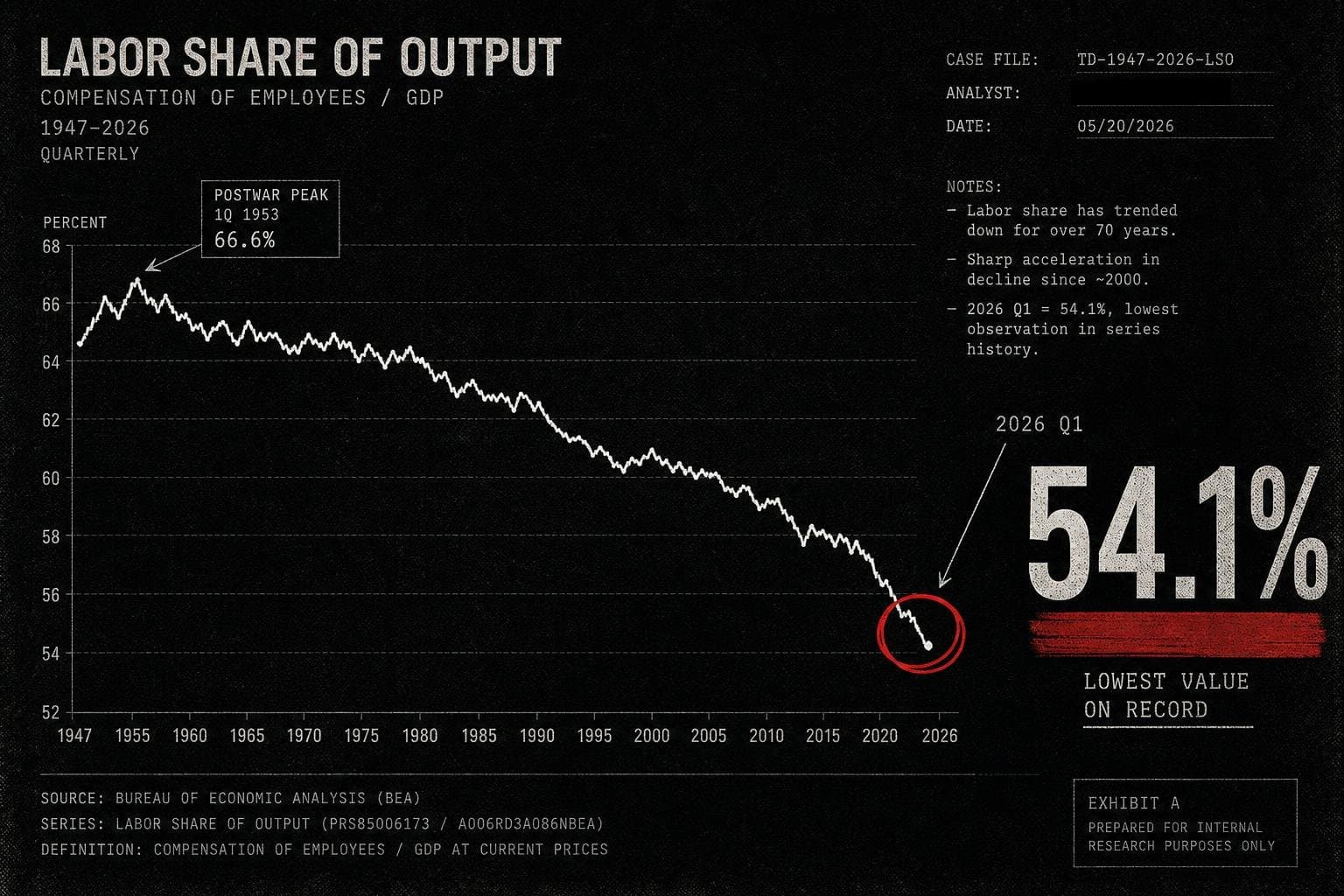

That's the labor share of output in Q1 2026 — the percentage of what the economy produces that flows back to workers as compensation. Per the BLS release, it is the lowest recorded value since the series began in 1947.

Not the lowest since the financial crisis. Not the lowest this decade. The lowest in the entire history of the measurement.

The Headline Number Obscures the Tension Inside It

Here's what the Q1 2026 data actually shows, and why the numbers don't fit together as neatly as the summary suggests:

- Productivity up 0.8% (Q1 2026, seasonally adjusted annualized rate) — output rose 1.5%, hours worked rose 0.7%

- Hourly compensation up 3.1% — sounds like workers are doing well

- Unit labor costs up 2.3% — compensation rising faster than productivity, which is inflationary pressure

- Real hourly compensation down 0.5% — once you adjust for consumer prices, workers lost ground in Q1

- Labor share: 54.1% — a record low

The apparent contradiction: compensation is rising in nominal terms, but workers are capturing a smaller share of output than at any point in 79 years of data. How?

The resolution is in the denominator. Output grew faster than compensation when measured as a share. Nominal wages going up doesn't mean workers are keeping pace with what they're producing — or with prices.

"Compared to What?" — The Four Comparisons That Matter

1. Compared to last quarter: Productivity grew 0.8% annualized. That's not a strong quarter. The year-over-year figure (2.9% from Q1 2025 to Q1 2026) is more flattering — but a single quarter's annualized rate and a four-quarter trailing rate are measuring different things. Don't conflate them.

2. Compared to the previous business cycle: The BLS release notes that since Q4 2019, productivity has grown at an annualized rate of 2.1% — above the 1.5% rate of the prior cycle (Q4 2007 through Q4 2019). That's a genuine improvement. It also doesn't tell us who captured the gains.

3. Compared to real wages: Real hourly compensation fell 0.5% in Q1. Over the last four quarters, it's up 1.4%. So workers are nominally ahead year-over-year, but behind in the most recent quarter — and structurally behind in terms of output share.

4. Compared to 1947: This is the one nobody is running with. The labor share series goes back to the postwar era. A record low in 2026 means workers are receiving a smaller fraction of what the economy produces than during any recession, any period of high unemployment, any era of weak union density in the modern data record. That's not a quarterly blip. That's a structural signal.

What the Data Doesn't Tell Us (And What People Will Claim It Does)

A few things to watch for as this number circulates:

- Causation claims: The record-low labor share will be attributed to automation, to trade policy, to union decline, to corporate consolidation — pick your prior. The BLS data shows the what, not the why. Correlation with any of those factors is not causation.

- The April jobs report: The April Employment Situation showed continued job growth, which will be used to argue the labor market is healthy. Both things can be true simultaneously — employment can be high while labor's share of output is at a record low. Headcount and share of output are different denominators.

- Nominal vs. real: Anyone citing the 3.1% compensation increase without the 0.5% real decline is doing the thing this newsletter exists to flag.

The Number to Watch in June

The BLS releases revised Q1 productivity figures and the Q2 preliminary data later this summer. The labor share figure will either stabilize or extend its trend. If it drops below 54%, that's not a data footnote — it's a structural story that every economic claim about worker prosperity will need to account for.

A record low that stays a record low for two consecutive quarters is no longer an outlier. It's a baseline.