The deal is nearly done. The lawsuits are being swatted away. The EU deadline is circled on the calendar. And yet the most consequential number in the Paramount-Warner Bros. Discovery merger story isn't the headline price tag — it's the two years of negative cash flow that S&P Global says the combined company should expect before the promised savings materialize.

That's the part of the merger narrative that tends to get buried under the antitrust drama.

The Legal Noise Is Mostly Just Noise

Paramount filed a motion this week to dismiss a federal lawsuit brought by five streaming subscribers who allege the merger violates antitrust law and will reduce their viewing options while raising prices. Paramount's response was characteristically blunt: the plaintiffs' allegations "do not have any factual support," and the whole thing is a "clumsy attempt to politicize antitrust litigation."

They're probably right that this particular lawsuit goes nowhere. Consumer antitrust suits of this type rarely survive a motion to dismiss, and Paramount's filing correctly notes that the plaintiffs are trying to unwind not just the WBD deal but the already-completed Skydance merger — a remedy courts are extremely reluctant to grant.

The more serious regulatory hurdle is in Brussels. Paramount has formally asked the EU to approve the $110 billion takeover of Warner Bros. Discovery, with a decision expected by July 7. European regulators have shown more appetite than their American counterparts for blocking or conditioning large media mergers, so that deadline is the one worth watching — not the California courthouse.

The Real Problem Is What Happens After Approval

Assume the deal clears. Then what?

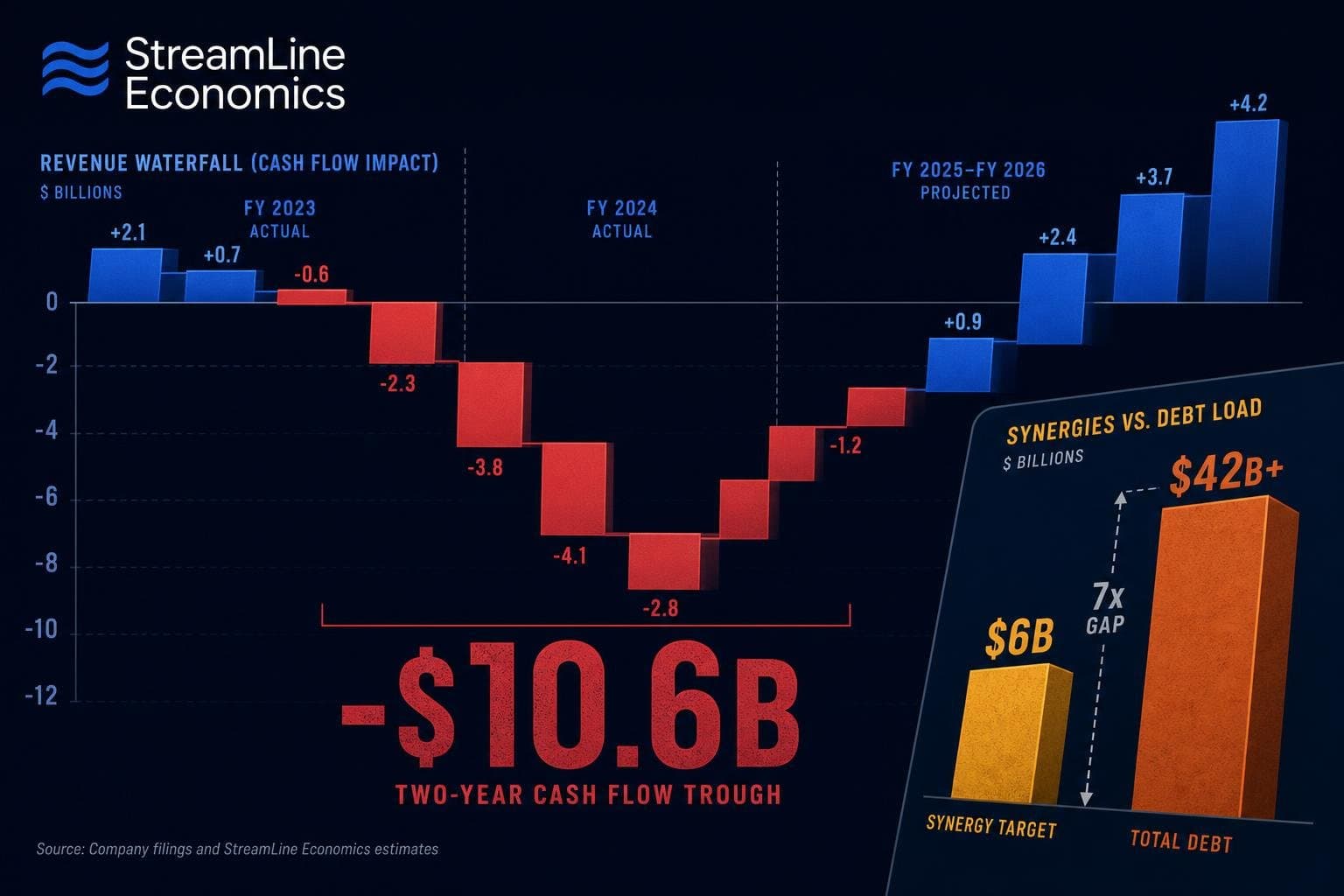

Naveen Sarma, S&P Global's sector lead for U.S. media and telecom, laid out the math on Variety's "Strictly Business" podcast: "Leverage is significantly high for this transaction." S&P downgraded the combined company's credit rating upon closing — a signal that the agency views the debt burden as a genuine constraint on the business, not just a technicality.

The company projects $6 billion in cost-cutting synergies, driven largely by technology upgrades, real estate consolidation, and operational efficiencies. Sarma says he believes the company can get there. But the timeline is the problem: "We're not going to see cash flow for probably the next two years."

Two years of constrained cash flow, while carrying the debt load of a $110+ billion transaction, while the linear TV business continues its structural decline, while streaming economics are still being figured out industry-wide. That's a narrow corridor to navigate.

The synergy story also deserves scrutiny. Sarma's framing — that cuts will come from technology and real estate rather than content spending — is the optimistic read. But every major media merger of the past decade has promised content-sparing synergies and then, when cash got tight, found that the easiest line item to cut was the one with the most flexibility: programming. The combined entity will control HBO Max and Paramount+, two services that will almost certainly need to be rationalized into something smaller. That rationalization has costs, and some of those costs will show up on screen.

The Broader Business Context These Deals Are Happening In

Here's what makes the timing interesting. The Paramount-WBD merger is being assembled at exactly the moment when the streaming business model is finally, genuinely working — just not for everyone.

Canada's broadcasting regulator recently announced rules requiring Netflix, Disney, and other large streamers to spend 15% of their annual Canadian revenue on local content, up from 5% — though Canada subsequently backed off that plan. The episode illustrates how regulators worldwide are watching the streaming profit era arrive and trying to extract a share of it before the window closes.

Meanwhile, analytics firm Antenna reports that ad-supported streaming subscriptions now represent 48% of all SVOD subscriptions in the U.S. — up from 39% two years ago — with 64% of first-time subscribers in Q1 choosing ad tiers. The dual revenue stream of subscriptions plus advertising is becoming the dominant model, which is good news for platforms that have scaled their ad businesses. It's less obviously good news for a newly merged company that will be spending the next two years trying to integrate two separate ad-tech stacks while managing a debt-heavy balance sheet.

Netflix and Disney have already done the hard work of building ad tiers and proving the model. The Paramount-WBD entity will be doing that integration work while simultaneously managing merger debt, regulatory conditions, and the ongoing collapse of linear TV revenue. That's not impossible. It is genuinely difficult.

What to Watch Before July 7

The EU decision is the near-term binary. If Brussels approves without significant conditions, the deal closes, the debt loads up, and the two-year cash flow clock starts. If the EU demands structural remedies — asset sales, licensing requirements, content access conditions — the economics of the merger change, and not in the combined company's favor.

Watch also for any signal about how the combined streaming service gets positioned. The branding and pricing decisions for a merged Paramount+/Max product will be the first real test of whether this entity can compete for subscribers in a market where nearly half of new sign-ups are choosing the cheapest option available.

The merger math only works if the streaming business grows faster than the debt compounds. That's the bet. The next six months will show whether it's a reasonable one.