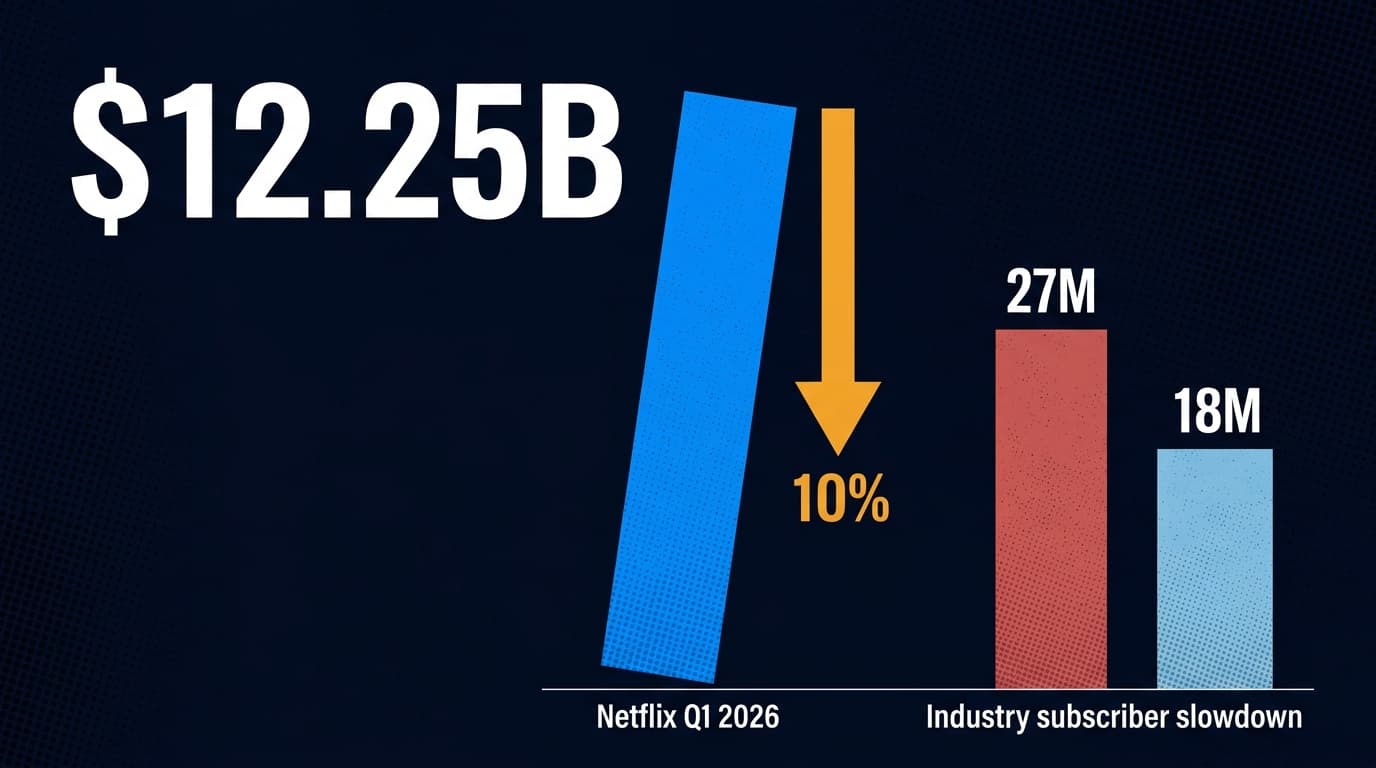

Netflix posted a genuinely strong quarter last week — $12.25 billion in revenue, up 16% year over year, with net income of $5.3 billion and free cash flow of $5.1 billion. Earnings per share came in at $1.23 against a Wall Street consensus of $0.76. By any conventional measure, that's a beat worth celebrating.

The stock fell 10% the next day.

That reaction isn't irrational. It's Wall Street telling you something about what Netflix's next chapter actually looks like — and the answer is murkier than the company's Q1 numbers suggest.

The Warner Exit Left a Strategy-Shaped Hole

The proximate cause of the selloff was soft Q2 guidance: Netflix projected 13% revenue growth for the April-June period, along with an operating margin of 32.6% — down from 34.1% in the year-ago quarter. The margin compression is partly mechanical: Netflix warned that content amortization costs would be front-loaded in the first half of 2026 before decelerating in H2. That's a timing issue, not a structural one.

But the harder question is strategic. Netflix spent months in serious talks to acquire Warner Bros. Discovery's studios-and-streaming business, offering $82.7 billion before walking away in February. Paramount ultimately won that deal. Now Netflix is the company that almost made a transformational bet on legacy content assets — and didn't. Analysts wanted to hear a clear alternative vision. They didn't get one.

BofA's Jessica Reif Ehrlich, who still rates the stock a buy, put it plainly: "In the first quarter following its decision to walk away from the Warner Bros acquisition, we would have expected a clearer and more compelling articulation of management's near- to medium-term outlook." That's analyst-speak for we're not panicking, but we're waiting.

Add Reed Hastings' announced departure from the board in June — ending a three-decade association with the company he co-founded — and you have a quarter where the numbers were fine but the narrative was unsettled.

The Broader Problem: Scale Is the Only Moat

Netflix's Q1 results look even stronger when you zoom out to the industry. Premium streaming subscription growth slowed to just 7% in 2025, adding roughly 18 million net new U.S. subscribers across all platforms — down sharply from 27 million the year before. The market is maturing, and the spoils are concentrating.

Netflix holds about 25% of U.S. premium streaming subscriptions. Disney+ sits at 14%, with 77% of its subscriber base now coming through bundles — a number that reveals both the power of the Disney-Hulu-ESPN package and the fragility of Disney+ as a standalone proposition. Peacock and Paramount+ are still fighting for relevance at the margins, their growth driven by individual title spikes rather than durable subscriber acquisition.

CNBC's analysis of Wall Street's streaming affections captured the dynamic cleanly: MoffettNathanson analyst Robert Fishman argued that streaming is a good business — "albeit only for those services with sufficient scale." That qualifier is doing a lot of work. At 280 million U.S. premium subscribers spread across a dozen platforms, "sufficient scale" increasingly means Netflix, and maybe Disney if the bundle holds.

What the Ad Tier Actually Means

One number buried in Netflix's Q1 letter deserves more attention: the company's ad-supported tier remains on track to reach $3 billion in revenue this year, doubling year over year. That's not a rounding error — it's a second revenue engine being built in real time.

The price increase Netflix announced in late March will show up more fully in Q2 results, not Q1. Combined with ad-tier growth, Netflix is running a dual monetization strategy that smaller competitors structurally cannot replicate: charge subscribers more and sell their attention to advertisers. Platforms without the subscriber density to attract premium ad rates are stuck choosing one lever or the other.

That's the real story underneath the stock drop. Netflix's Q1 was strong. Its Q2 guidance was soft. Its strategic narrative after the Warner exit is incomplete. But the underlying economics — scale, dual monetization, international growth running at 19-20% in Latin America and Asia-Pacific — remain intact in ways that most of its competitors can only approximate.

Watch for Q2 earnings in mid-July. That's when the price increase impact becomes visible in the revenue line, and when management will face the same question again: what does Netflix become now that the Warner deal is off the table? The numbers will be fine. The answer to that question is what the stock is actually pricing.