The Inflation Reduction Act was sold, in part, on a simple promise: federal dollars would buy meaningful emissions reductions at a defensible price. The math is getting less defensible.

The Numbers Have Moved — Not in the Right Direction

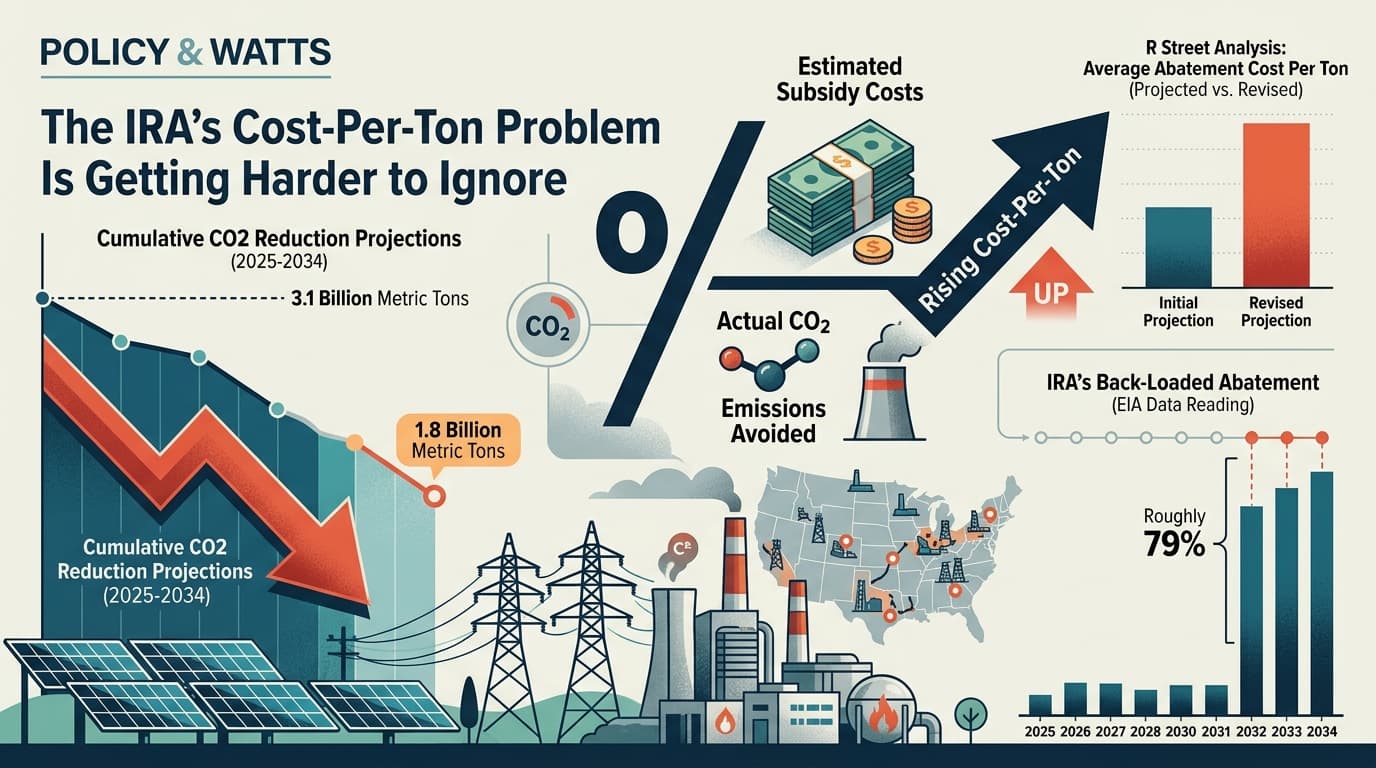

When the EIA first modeled the IRA's energy subsidies in 2023, it projected cumulative CO2 reductions of 3.1 billion metric tons from 2025 through 2034. Updated 2025 projections cut that figure to 1.8 billion metric tons — a 42% reduction in projected abatement, against a subsidy cost that hasn't shrunk proportionally.

That's the core of the cost-per-ton problem. If the denominator (tons avoided) falls while the numerator (dollars spent) holds steady or rises, the abatement cost per ton climbs. R Street's analysis of EIA data puts this plainly: the IRA's average abatement cost has risen as near-term emission reductions have underperformed initial projections.

There's a compounding issue in the timing. According to R Street's reading of EIA data, roughly 79% of the IRA's projected abatement is now expected to occur in the final three years of the 2025–2034 window. That's a lot of weight resting on long-range projections that already proved optimistic once. If the near-term miss is any guide, the back-loaded abatement numbers deserve skepticism.

Why Near-Term Abatement Underperformed

The EIA's revised projections reflect a few converging realities. First, 2022 emissions came in roughly 87 million metric tons above what had been projected — a higher baseline that makes displacement harder to measure and claim. Second, the anticipated pace at which IRA subsidies would displace fossil fuel use has slowed in the near term. This isn't necessarily a fatal flaw in the policy design; subsidy programs often take years to move capital at scale. But it does mean the early cost-per-ton figures are running high.

The EIA's AEO2026 adds context here: electricity demand growth is accelerating, driven substantially by data centers. When demand grows faster than clean capacity can be built, the marginal unit of electricity often comes from existing fossil generation. Subsidizing new renewables while demand surges can mean you're adding clean capacity without actually retiring dirty capacity — the grid absorbs both. The environmental accounting gets murkier.

What This Doesn't Mean

None of this is an argument that the IRA subsidies are worthless. Cost-per-ton calculations at this stage are inherently rough — they depend on baseline assumptions, discount rates, and projections that will be revised again. The R Street analysis is transparent about its methodology's limits, including the absence of an updated no-IRA scenario from EIA.

What it does mean is that the subsidy-effectiveness question deserves more rigorous ongoing tracking than it typically receives. The political debate around the IRA tends to collapse into either "historic climate investment" or "wasteful spending" — neither of which is analytically useful. The more productive frame is: which specific programs within the IRA are delivering abatement at what cost, and how does that compare to alternatives?

Solar and wind production tax credits, EV credits, and industrial decarbonization incentives all have different cost structures and different abatement profiles. Treating the IRA as a single number obscures which parts are working and which are expensive ways to feel good about the energy transition.

What to Watch

The IRA's subsidy provisions are already under political pressure from the current administration and congressional budget negotiations. Whatever happens legislatively, the more important analytical moment will come when EIA releases updated no-policy scenarios — which would allow a cleaner isolation of subsidy effects from broader market shifts in fuel prices and technology costs.

Watch also for Treasury's ongoing IRA implementation guidance, which shapes which projects actually qualify for credits and at what value. The gap between authorized spending and actual credit claims will be the first real signal of whether the back-loaded abatement projections have any grounding in deployment reality.

The IRA may still deliver on its emissions promises. But "may still deliver" is a different claim than the one made in 2022 — and the cost per ton of that delivery is a number worth tracking every time EIA updates its models.