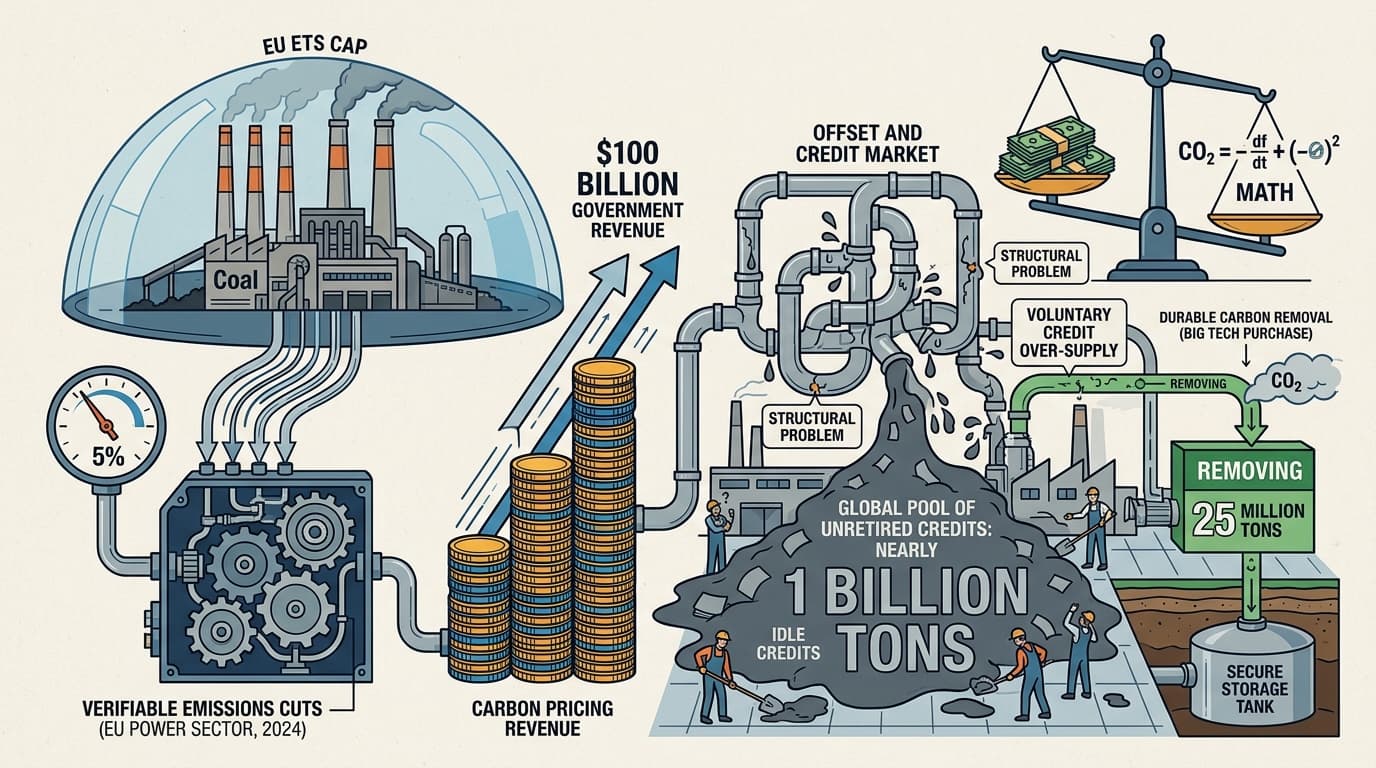

Global carbon pricing crossed $100 billion in government revenue for the second consecutive year in 2024, according to the World Bank's State and Trends of Carbon Pricing 2025. That's a clean headline. The underlying numbers are considerably less tidy.

The revenue story is real: compliance markets — emissions trading systems and carbon taxes — are functioning as fiscal instruments. Governments are collecting. But the World Bank's own data flags a structural problem on the offset side: carbon credit supply continued to outstrip demand in 2024, pushing the global pool of unretired credits to nearly 1 billion tons. A billion tons of credits sitting idle isn't a sign of a market working efficiently — it's a sign that demand for offsets isn't keeping pace with the volume being issued.

The EU's compliance market tells a cleaner story. EU ETS emissions fell 5% in 2024, driven primarily by cuts in the power sector, and the system remains on track toward its 2030 target. That's a measurable outcome: a cap-and-trade system with a hard ceiling producing verifiable reductions. The mechanism works when the cap is tight and enforced.

The voluntary carbon market is a different animal. Big Tech's push into carbon removal credits is creating a bifurcated market — durable carbon removal purchases jumped from 8 million tons in 2024 to 25 million tons so far in 2025, according to Lukas May, chief commercial officer at a carbon removal firm. That growth is real, but it's concentrated in a premium tier that represents a fraction of total credit volume. The bulk of the voluntary market — older forestry and cookstove credits — remains oversupplied and underscrutinized.

The pattern suggests two carbon markets operating under the same branding. Compliance systems with hard caps are generating both revenue and measurable emission reductions. Voluntary offset markets are generating revenue and a growing inventory of unretired credits whose actual climate impact varies enormously by project type and vintage. Who's making money? Governments collecting ETS auction revenue, and increasingly, durable removal project developers riding Big Tech demand. Who's actually offsetting CO2 at scale? Primarily the compliance systems — where the accounting is mandatory, audited, and tied to a declining cap.

The $100 billion figure will keep growing. Whether the ton-for-ton offset math holds up depends almost entirely on which part of the market you're measuring.