The International Space Station has been continuously occupied since November 2000. That unbroken human presence in low Earth orbit — now stretching across a quarter century — is easy to take for granted. It's also, depending on how the next decade unfolds, not guaranteed to continue.

NASA plans to retire the ISS around 2030-2031 and replace it with commercially operated stations through its Commercial LEO Development (CLD) program. The pitch is straightforward: let private companies build and operate the infrastructure, while NASA buys access as a customer rather than running the whole operation. Lower costs, more flexibility, broader access. That's the theory. The engineering and business realities are considerably messier.

What's Actually Being Built — and What Isn't Yet

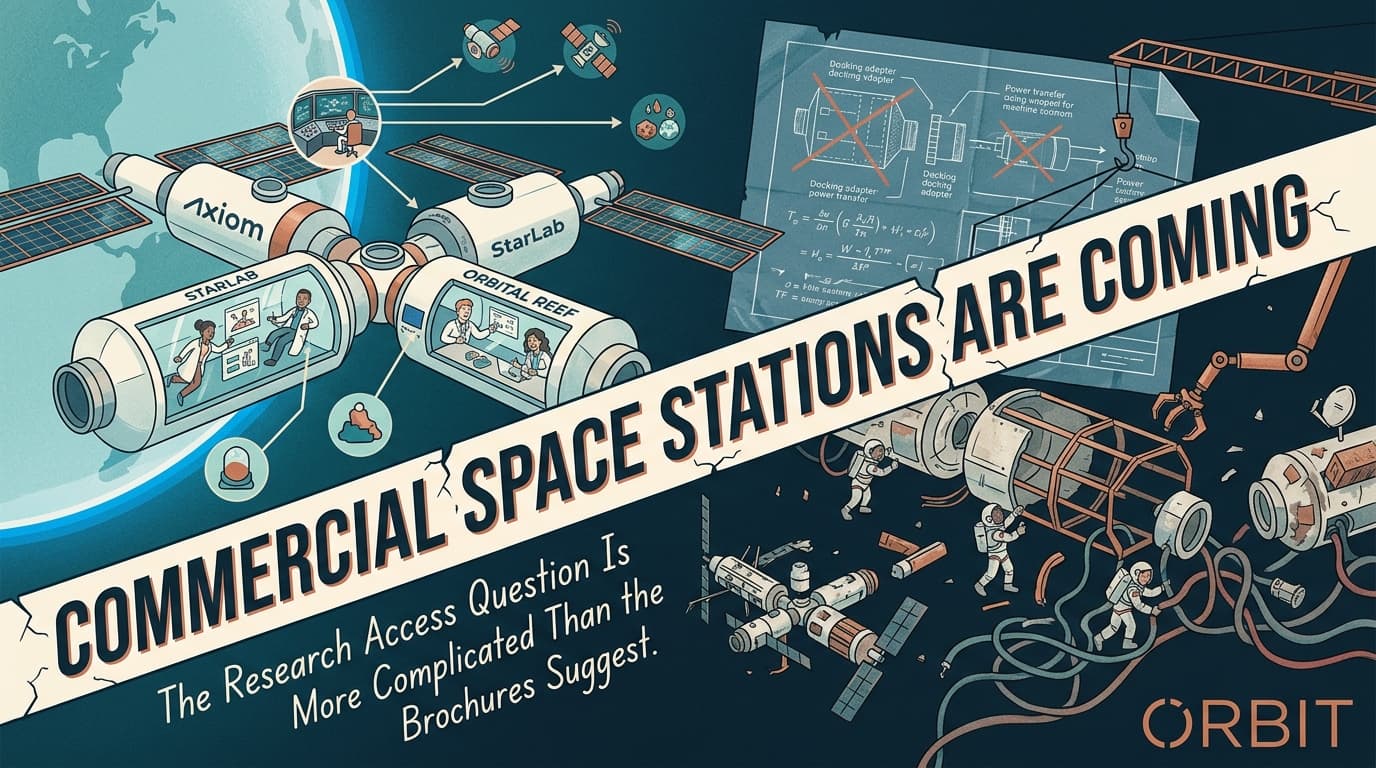

Four main contenders are in various stages of development. Axiom Space has the most concrete foothold: it received a NASA award in 2020 to attach at least one module to the ISS, giving it a path to operational experience before flying solo. Starlab, a joint venture involving Voyager Space and Airbus, is pushing through detailed design work. Orbital Reef, the Blue Origin-led consortium, is described as lagging behind the other contenders. And Vast has emerged as a faster-moving dark horse, with ambitions that have surprised some observers.

The critical program milestone is NASA's Phase 2 certification award, currently planned for mid-2026. That's when NASA selects which destination — or destinations — will receive official certification and operational service contracts. Everything before that is still proposal territory.

Here's the uncomfortable gap in the timeline: the ISS retirement is targeted around 2030-2031, and NASA's own Low Earth Orbit Microgravity Strategy acknowledges that the commercial transition might leave gaps in continuous human presence. Going from certification award in 2026 to an operational, crewed station by 2030 is an aggressive schedule for any of these programs. The pattern in commercial space development — ambitious timelines meeting hardware reality — should make anyone cautious about assuming a seamless handoff.

The Research Access Question Nobody's Answering Clearly

The promotional framing around commercial stations emphasizes democratized access — more researchers, more companies, more nations able to buy time on orbit without going through NASA's allocation process. That's a real potential benefit. The ISS research queue has always been constrained, and a commercial model could, in principle, open the pipeline.

But the actual research access picture depends on details that aren't settled yet.

On the ISS, NASA and its international partners fund the station's operations and in return get research time allocated through government processes. Researchers apply, proposals get reviewed, and access is rationed. It's bureaucratic, but the cost of the underlying infrastructure is absorbed by the agencies. On a commercial station, the operators need to cover their costs — which means research time has a market price attached to it.

NASA's CLD program intends for the agency to purchase crew time and research capacity as an anchor customer, which would preserve some government-funded research access. But the fraction of station capacity NASA actually buys — versus what gets sold commercially to pharmaceutical companies, materials science firms, or space tourism clients — will determine whether the research environment resembles the ISS or something closer to a high-end orbital hotel with a lab module attached.

The honest answer is that nobody knows yet, because the business models aren't finalized and the certification awards haven't been made. What the proposals mean for orbital research access is largely a function of contract terms that will be negotiated over the next two to three years.

The China Factor

One context that doesn't appear in the commercial station brochures but shapes the strategic picture: China's Tiangong station is operational and expanding its presence. If the U.S. commercial transition produces a multi-year gap in crewed LEO capability, the geopolitical optics are significant — and that pressure is part of why NASA has been pushing the CLD program forward even as budgets tighten.

That urgency is worth tracking. Programs that are politically motivated to succeed on a fixed timeline don't always make better engineering decisions because of it.

Also Worth Watching

Artemis II prep continues. NASA published its daily mission agenda for Artemis II, the first crewed lunar flyby mission. The level of published operational detail signals the mission is moving from planning into execution mode. No launch date confirmed in the available sources, but the cadence of crew-facing documentation is a reasonable indicator of program maturity.

Webb keeps delivering. NASASpaceFlight reports that Webb has revealed new structures in a planetary nebula, continuing its run of observations that push into territory ground-based telescopes simply can't reach. Each result like this is a reminder of what the instrument was actually built for — not the headline-grabbing deep field images, but the systematic science of understanding how stars end and what they leave behind.

The commercial station transition is real, the timeline is tight, and the research access implications are genuinely unresolved. The mid-2026 certification decision is the next concrete moment when the picture will sharpen. Until then, the gap between the promotional vision and the operational reality is worth keeping in mind every time a new rendering of a gleaming orbital habitat shows up in your feed.