The most interesting spread in sports betting this week isn't between DraftKings and FanDuel on an NFL line. It's between two legal realities: one where prediction markets are regulated financial instruments operating freely, and another where they're criminal enterprises. That gap — jurisdictional, regulatory, and structural — is actively reshaping where odds get made, who makes them, and how much friction exists between platforms. For cross-market arbitrage, the infrastructure story matters as much as the line movement.

Section 1: The Regulatory Fault Line Splitting the Market

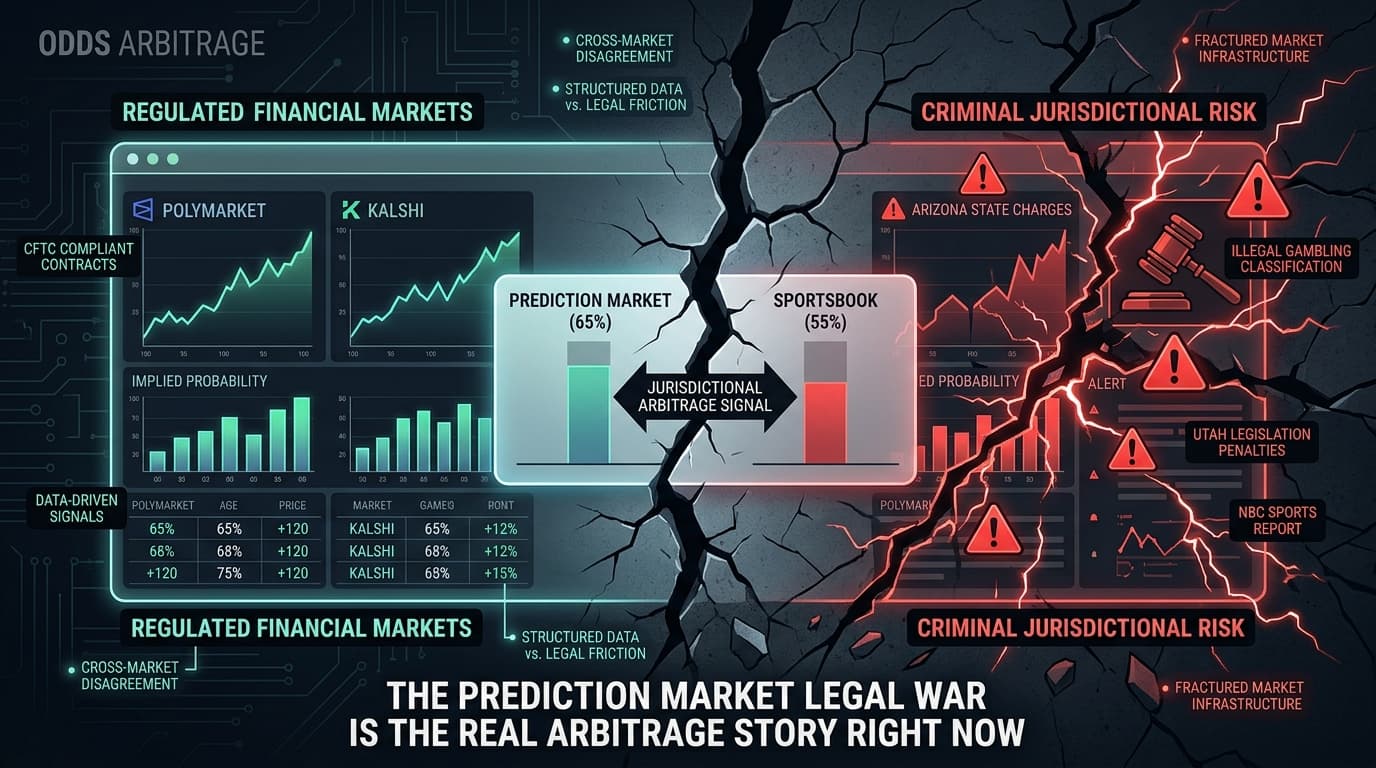

Kalshi is facing criminal charges in Arizona for running what prosecutors are characterizing as an illegal gambling business. NBC Sports reported the charges, making it one of the most direct legal confrontations a prediction market platform has faced at the state level. This isn't a cease-and-desist or a regulatory inquiry — it's criminal exposure.

The Arizona situation doesn't exist in isolation. Utah is pursuing parallel legislative action, with bills specifically designed to stop prediction markets from operating in the state. Greenwich Time reported that Utah's legislation also targets FanDuel and DraftKings, which have built their own prediction market products — a move analysts say could allow those companies to route around state gambling prohibitions. The Utah legislature is treating the sportsbook-adjacent prediction market products as functionally identical to traditional gambling, regardless of how they're structured at the federal level.

This creates a direct market structure problem. When a platform faces criminal exposure in one state and legislative prohibition in another, liquidity fragments. Users in affected states either exit the market or migrate to platforms with cleaner legal standing. That migration doesn't happen uniformly — it happens in waves, tied to news cycles and enforcement actions. Each wave creates temporary pricing dislocations between platforms, because the user base composition shifts faster than the odds algorithms adjust.

The practical implication: when Kalshi faces a major legal headline, watch for short-term divergence between Kalshi-listed contracts and equivalent markets on Polymarket or traditional sportsbooks. The dislocation is real, but it's time-sensitive.

Section 2: The CFTC Is Trying to Build a Bridge — But It's Incomplete

While state prosecutors are treating prediction markets as gambling operations, the federal regulator is moving in the opposite direction. Forbes reported that the CFTC is actively urging prediction markets to partner with sports leagues — a signal that the federal framework wants to formalize and legitimize the sector rather than restrict it.

That federal-state tension is the core structural issue. Kalshi and Polymarket operate under CFTC jurisdiction as designated contract markets or exempt platforms. Their legal theory is that sports event contracts are commodity futures, not gambling products. States disagree. Arizona's criminal charges represent the sharpest version of that disagreement yet.

The CFTC's push toward league partnerships is notable because it suggests the agency sees legitimization through data-sharing and official relationships as the path forward. If prediction markets can demonstrate they're operating with league cooperation — accessing official data feeds, maintaining integrity agreements — the argument that they're gambling operations becomes harder to sustain in state courts.

But that bridge isn't built yet. Right now, the gap between federal permissiveness and state enforcement creates a two-tier market. Platforms with strong CFTC relationships and national user bases price events one way. State-regulated sportsbooks, constrained by local licensing requirements and different user demographics, price them another. That's the seam where cross-market discrepancies live.

Section 3: Where the Odds Diverge — Entertainment Markets as a Case Study

The structural tension between prediction markets and sportsbooks shows up most clearly in entertainment markets, where the two ecosystems have historically priced things very differently. The 2026 Oscar markets currently running across platforms illustrate the point.

FanDuel's Best Picture market has One Battle After Another at -500, implying roughly 83% probability. Sinners sits at +340, implying about 23%. Those two numbers already sum past 100% — standard vig — but the gap between the heavy favorite and the field is steep.

DraftKings' Best Actor market shows Michael B. Jordan at -185 (65% implied) versus Timothée Chalamet at +180 (36% implied). That's a relatively tight two-horse race by sportsbook standards. Kalshi's Best Actress market is the most extreme: Jessie Buckley at -4000 implies 97.6% probability — a market that has essentially closed.

The divergence pattern here is instructive. Sportsbooks tend to keep more liquidity in the field because recreational bettors want options and long shots. Prediction markets, with more sophisticated user bases, collapse toward consensus faster. When Kalshi shows 97%+ on a single outcome and a sportsbook is still offering +800 on the second choice, that's not necessarily mispricing — it may reflect different user bases reaching different equilibria. But when the gap is that wide, it's worth examining which market has better information flow.

Entertainment markets are also where the legal friction matters least — neither Arizona nor Utah's enforcement actions are primarily targeting Oscar contracts. That makes them cleaner test cases for pure cross-market pricing analysis, without the liquidity distortion that comes from users fleeing a platform due to legal risk.

Section 4: The Structural Arbitrage Thesis Going Forward

The through-line across all of this is that prediction market arbitrage in 2026 isn't just about finding a 10-point spread between Polymarket and DraftKings on an NFL game. The bigger opportunity — and the bigger risk — is structural. Legal fragmentation is creating persistent pricing differences that won't resolve through normal market efficiency mechanisms, because the markets themselves can't fully integrate.

When Kalshi faces criminal exposure in Arizona, its Arizona user base shrinks or exits. The remaining users may be more sophisticated, which could make Kalshi's prices more accurate — or they may be more risk-tolerant, which could make them more aggressive. Either way, the composition shift changes the price. A sportsbook operating legally in Arizona, with a full retail user base, will price the same event differently. That difference isn't noise — it's signal about which market is under structural stress.

The CFTC's push for league partnerships suggests the federal framework is moving toward consolidation and legitimization. If that process accelerates — official data feeds, league agreements, cleaner regulatory standing — the friction between prediction markets and sportsbooks decreases, and with it, the persistent structural discrepancies. The arbitrage window on this particular seam has a clock on it.

The near-term playbook: track legal developments in Arizona and Utah as leading indicators of platform liquidity stress. When enforcement actions hit, watch for 48-72 hour windows where affected platform prices lag market consensus. That's when the cross-market spread is most likely to be actionable rather than reflective of genuine information asymmetry. The legal war is the market signal. Read it accordingly.