There's a structural fault line running through sports betting right now, and most bettors are standing on the wrong side of it.

Prediction markets and traditional sportsbooks have always priced the same events differently — different user bases, different liquidity pools, different regulatory frameworks shaping what can even be offered. That divergence has historically been narrow enough to treat as noise. But something shifted in the last several months. Prediction markets aren't just growing; they're being formally integrated into the sports ecosystem in ways that change how information flows, how quickly lines move, and — critically — where the pricing gaps open up. The MLB-Polymarket partnership announced this week is the clearest signal yet that these two market types are converging structurally while remaining divergent in price. That combination is exactly where arbitrage lives.

This issue is about that seam: how it formed, why it persists, what the regulatory pressure building against it means for traders, and where the actionable signals are pointing right now.

How the Seam Formed: Two Markets Pricing the Same Reality Through Different Lenses

To understand why Polymarket and DraftKings can look at the same game and produce meaningfully different implied probabilities, you have to understand that they aren't really the same product serving the same customer.

Traditional sportsbooks — DraftKings, FanDuel, BetMGM — are built around sharp line management. They employ traders whose job is to move lines fast when information changes, and they're working with decades of infrastructure for absorbing sharp action and adjusting. Their user base skews toward recreational bettors on one end and professional arbitrageurs on the other, with the book managing both by shading lines and limiting winners. The result is a market that's often efficient on major events but can lag on secondary markets, player props, and anything that requires integrating information from outside the traditional injury report pipeline.

Prediction markets operate differently. Polymarket runs on a decentralized model where users are essentially trading binary contracts — yes/no outcomes — and the price reflects aggregate user belief rather than a book's managed line. The user base skews toward crypto-native traders, political forecasters, and a growing cohort of sports bettors who've discovered that Polymarket's interface lets them express views that sportsbooks won't take. Crucially, Polymarket has historically been faster to integrate novel information — not because its users are smarter, but because the platform doesn't have the same incentive to shade lines away from sharp action.

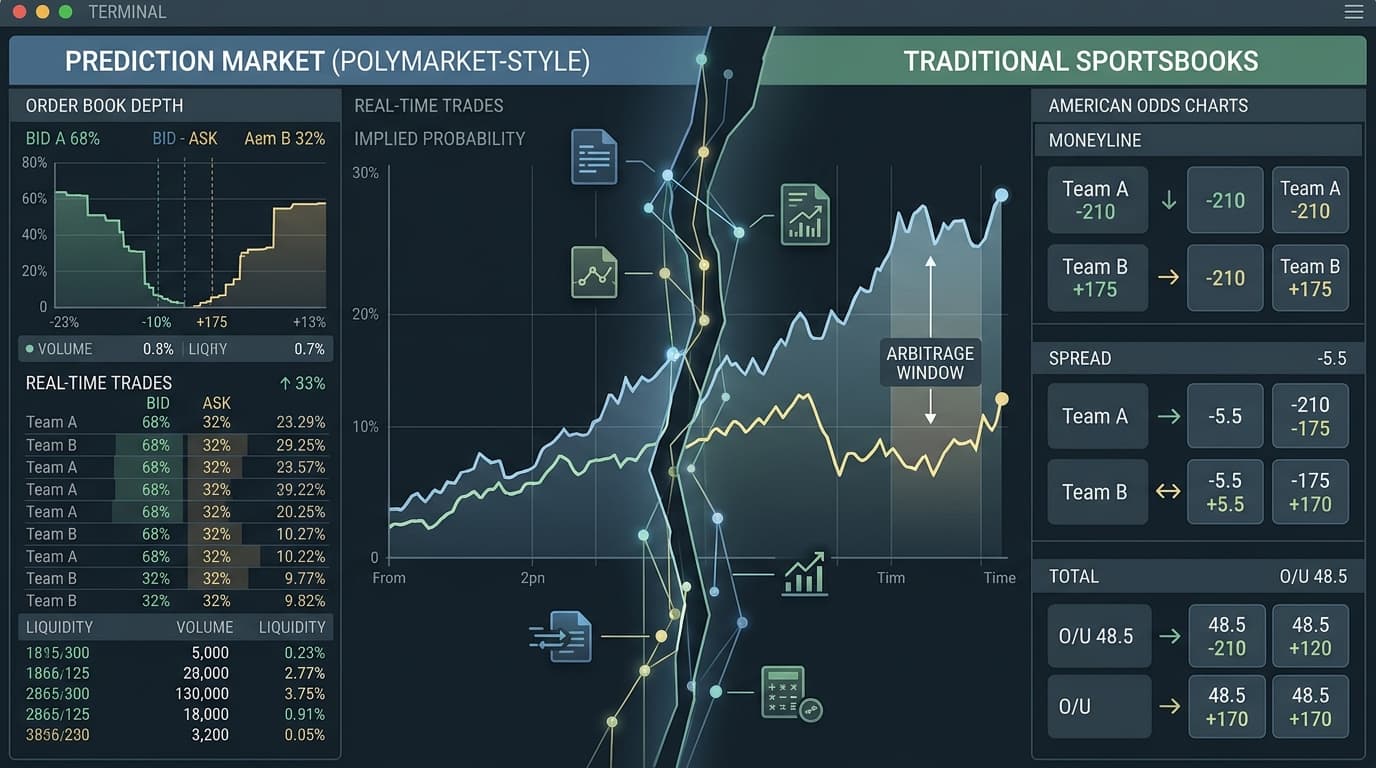

That structural difference produces pricing gaps. When injury news breaks, Polymarket often moves before sportsbooks because there's no book risk to manage — the platform just reflects what traders believe. When a sportsbook has a liability imbalance on one side of a game, it shades the line in ways that Polymarket doesn't. When a game involves a market that sportsbooks offer with limited liquidity (think: specific player props, niche soccer leagues, early-week NFL futures), Polymarket's contract prices can diverge significantly from the implied probability embedded in the sportsbook line.

The MLB deal formalizes something that was already happening informally. MLB named Polymarket its official prediction market exchange, a partnership that comes with official data licensing through Sportradar. That data pipeline matters: Sportradar is not bound by exclusivity between MLB and Polymarket, meaning it can still supply MLB data to traditional sportsbooks and other platforms. But the formal relationship between Polymarket and MLB creates a different kind of information adjacency — one where Polymarket's contracts may reflect official data faster, or with greater precision, than what's embedded in a DraftKings line set by a trader managing book exposure.

MLB is not the first league to move in this direction. The NHL signed licensing deals with both Polymarket and Kalshi in October, and Polymarket already holds marketing agreements with MLS and UFC. What's notable is what's missing: the NFL and NBA remain holdouts. Those are the two highest-liquidity sports betting markets in the United States, and their absence from prediction market partnerships is itself a signal — one we'll return to.

The Mechanism: Why Gaps Open, and Why They Don't Close Instantly

A 10-point spread between a Polymarket implied probability and a DraftKings line doesn't persist because one market is stupid. It persists because the friction costs of closing it are real, and because the two markets are drawing on different information at different speeds.

Here's the basic mechanism. Polymarket prices a game at 62% for the home team. DraftKings has the same team at -130, which converts to roughly 56.5% implied probability after vig. That's a 5.5-point gap — not quite the 8-10 point threshold where the signal gets cleanest, but worth watching. The question isn't which market is right; it's why they disagree and whether the disagreement is closing or widening.

Several things can cause that gap to open:

Injury information asymmetry. Polymarket traders are often faster to price in injury news because they're monitoring the same social feeds and beat reporters as everyone else, but without a book's lag time for line adjustment. When a starting pitcher's availability is uncertain the morning of a game, Polymarket contracts can move 8-12 points before DraftKings adjusts its moneyline. That window is usually short — 20 to 40 minutes — but it's real.

User base composition. DraftKings' recreational user base creates systematic biases. Favorites are consistently overbet by recreational players, which means books shade lines toward the underdog to balance liability. Polymarket's user base, being more analytically oriented, doesn't exhibit the same favorite-longshot bias to the same degree. The result: on games with heavy public action toward a favorite, Polymarket will often show a lower implied probability for that favorite than DraftKings — not because Polymarket is right, but because DraftKings is managing liability rather than expressing a pure probability estimate.

Liquidity gaps on secondary markets. The biggest pricing divergences don't happen on NFL moneylines or NBA spreads — those markets are too liquid and too heavily arbitraged. They happen on player props, game totals in lower-profile matchups, and futures markets where sportsbook liquidity is thin. Polymarket's contract structure lets it offer markets that sportsbooks won't touch, and when both platforms offer the same market with different liquidity depths, the prices can diverge substantially.

Regulatory structure. This is the least-discussed driver of pricing gaps, but it's increasingly important. Polymarket operates under CFTC oversight as a derivatives exchange, not under state gaming regulations. That means it can offer markets in states where DraftKings can't, and it can structure contracts in ways that don't map cleanly onto traditional sportsbook offerings. When the regulatory frameworks diverge, the user bases diverge, and when the user bases diverge, the prices diverge.

The MLB-Polymarket deal is accelerating this dynamic. By formalizing the data relationship, it creates a pathway for Polymarket to receive and integrate official league data faster and more reliably than it could through third-party aggregators. If Polymarket's contracts are priced on official data while a sportsbook's line is still catching up to the same information, the gap widens — and the direction of the gap becomes more predictable.

The Tension: A Senate Bill That Could Collapse the Seam Entirely

Here's the complication that every prediction market trader needs to be tracking right now, because it's the single biggest structural risk to the cross-market arbitrage thesis.

In March, Senators Adam Schiff and John Curtis introduced the "Prediction Markets Are Gambling Act," which would prevent CFTC-registered entities from listing any prediction contract that resembles a sports bet. The bill, reported by The Athletic, is bipartisan — which makes it more dangerous than the typical single-party regulatory threat. Kalshi and Polymarket have both moved to implement insider trading controls in apparent response to the regulatory pressure, signaling that they're taking the legislative risk seriously.

If the bill passes in anything like its current form, it would effectively end sports prediction markets as a distinct asset class in the United States. Polymarket would no longer be able to list contracts on NFL game outcomes, MLB series results, or NBA championship futures. The pricing gap between prediction markets and sportsbooks wouldn't narrow — it would disappear, because one side of the trade would cease to exist.

That's the tail risk. But the more immediate tension is subtler: the bill's existence is already affecting how prediction market platforms behave, and that behavioral change is affecting pricing.

Polymarket and Kalshi implementing insider trading controls means they're adding friction to the information flow that makes prediction markets fast. If a team executive knows a star player is sitting out and trades on that information through a Polymarket contract, the new controls are designed to catch and reverse that. That's good for market integrity, but it also means Polymarket loses some of its information-speed advantage over sportsbooks. The gap may narrow not because sportsbooks get faster, but because prediction markets get slower.

There's also a liquidity effect. Regulatory uncertainty suppresses participation. Traders who might otherwise build positions in Polymarket sports contracts are sitting on the sidelines while the legislative picture clarifies. Lower liquidity means wider bid-ask spreads, which means the apparent pricing gaps are partly an artifact of thin markets rather than genuine information divergence. Distinguishing between a real gap and a liquidity-driven gap is one of the harder analytical problems in cross-market arbitrage right now.

The league partnership dynamic adds another layer. The NFL and NBA are holdouts from prediction market deals — and that's not an accident. As noted in Gaming America's coverage, those two leagues are watching the regulatory situation before committing. If the Schiff-Curtis bill gains traction, the NFL and NBA will have been right to wait. If it fails, expect both leagues to move quickly — and when they