The U.S. military's satellite communications architecture just got a lot more interesting. Within the span of two weeks, the Space Force committed over $2.7 billion across two structurally different programs — and the companies winning the work tell you exactly what the Pentagon is actually trying to solve.

The short version: the military is no longer betting on a single satellite network to carry tactical communications. It's building layered redundancy by design, and the startup ecosystem is finally mature enough to supply the hardware.

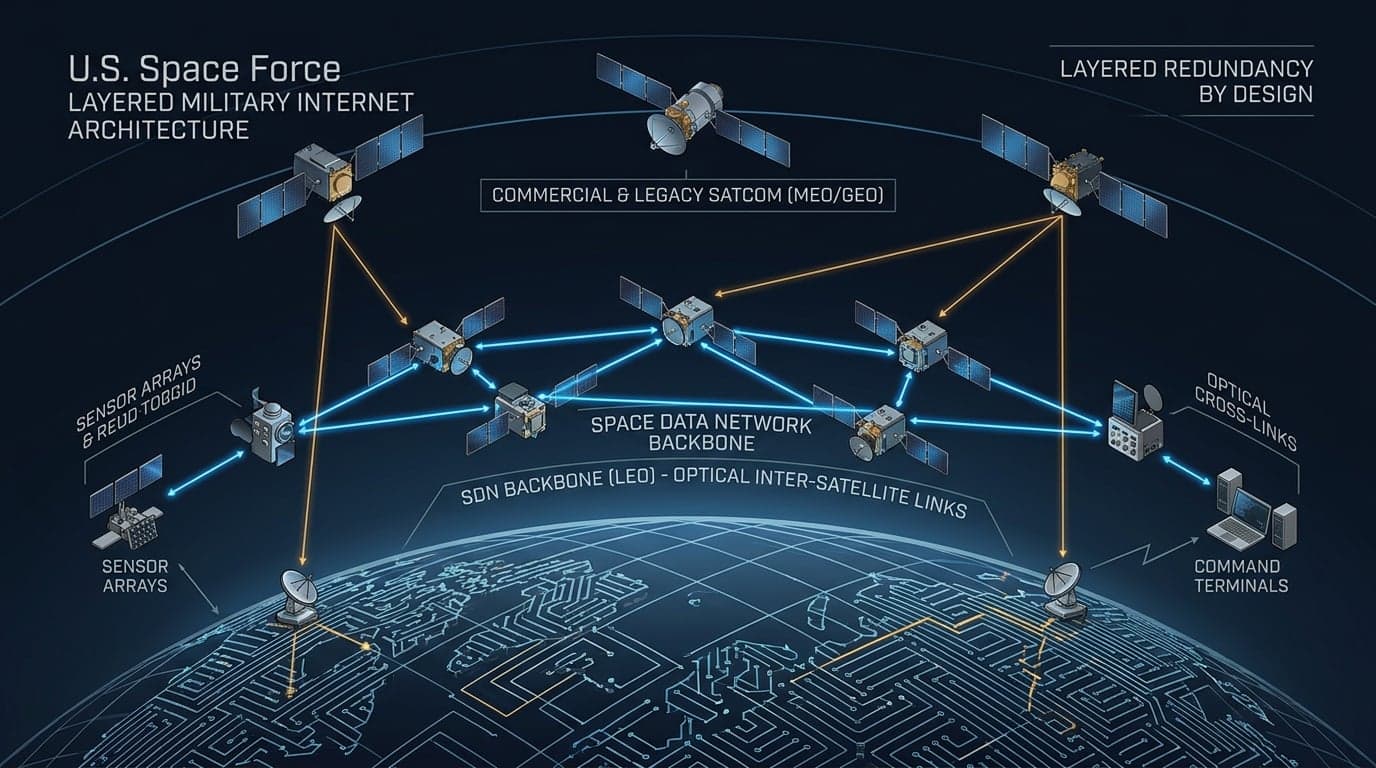

The Two Bets Running in Parallel

On May 26, SpaceX won a $2.29 billion Space Force contract to build the Space Data Network Backbone — a constellation of optically interconnected low Earth orbit satellites designed to move military data through space rather than routing it through ground stations. Previously called MILNET, the SDN Backbone is explicitly the "backhaul" layer: high-capacity data transport between spacecraft, sensors, command systems, and weapons platforms. SpaceX will build it using Starshield, its government-focused Starlink variant, but the Space Force will operate the constellation.

Then, on June 9, the Space Force announced a separate $437.7 million award to Viasat and SES for the Protected Tactical SATCOM-Global program — two geostationary satellites designed specifically for anti-jam communications in denied environments. PTS-G uses the Protected Tactical Waveform, a military-specific anti-jam protocol, and maintains backward compatibility with legacy tactical SATCOM systems. It operates in X-band and military Ka-band. Space Systems Command's acting portfolio acquisition executive framed the program as designed to "ensure connectivity in denied environments" — the explicit scenario where adversaries are actively trying to sever the link.

These are not competing programs. They're solving different problems in the same architecture. The SDN Backbone is about throughput and speed at scale. PTS-G is about survivability when someone is jamming you.

Where the Startups Actually Fit

The PTS-G contract awards look like they went to established operators — Viasat and SES are not exactly scrappy newcomers. But SpaceNews reported that the spacecraft buses underneath those satellites are being built by K2 Space and Rocket Lab. K2 Space, a California-based startup, is providing the satellite platform for SES's entry. Rocket Lab is supplying the spacecraft bus for Viasat's satellite.

This is the pattern worth tracking. The primes win the headline contract. The startups win the structural work that determines whether the satellite actually performs. K2 Space in particular is extending a relationship it already had with SES — the company was previously selected to provide spacecraft buses for SES's commercial broadband constellation, giving it a credible track record before the military contract materialized.

That's the repeatable success factor I've tracked across this publication's coverage of defense procurement: startups that enter the defense supply chain through commercial adjacencies — building real hardware for real customers — arrive at the Pentagon door with something more valuable than a pitch deck. They have flight heritage. The DIU's own competitive contracting model reinforces the same logic: demonstrated capability in adjacent domains is the fastest path to a military contract, whether you're building drone propulsion or satellite buses.

The Concentration Risk Nobody Is Ignoring

The SDN Backbone award to SpaceX generated immediate concern, and the Space Force acknowledged it directly. The earlier Space Development Agency Transport Layer program distributed procurement across multiple vendors — SDA has contracted for more than 300 Transport Layer satellites through its Tranche 1 and Tranche 2 awards. The Pentagon restructured the effort before Tranche 3, shifting emphasis toward the SDN and concentrating a major portion of future satellite procurement under a single company.

The Space Force's answer — that additional vendors are expected to participate in the broader SDN architecture over time — is the right institutional response, but it's also a placeholder. The real test is whether the acquisition framework actually opens competitive on-ramps for other LEO operators, or whether SpaceX's cost and integration advantages make that language functionally meaningless.

This is where the PTS-G model is instructive. The Space Force ran PTS-G as a genuinely competitive acquisition — two separate awards, two different prime contractors, two different startup bus suppliers. Space Systems Command explicitly cited "commercial innovation through a competitive acquisition approach" as the program's design intent. That's not just procurement language. It's a structural choice that keeps the industrial base alive and gives K2 Space and Rocket Lab a reason to keep investing in military-grade hardware.

The concentration concern isn't unique to space. Reuters reported this week that European defense planners are wrestling with the same tension in autonomous aircraft — four companies competed at the Berlin airshow for wingman drone contracts, precisely because no government wants a single-vendor dependency on a platform that has to work when adversaries are actively contesting the environment. The structural logic is identical: resilience requires competition, not just redundancy.

What the Next 18 Months Reveal

The PTS-G Swarm 1 satellites are expected to enter service in 2029. The SDN Backbone is earlier-stage. The real signal to watch isn't the launch dates — it's whether the Space Force follows through on competitive awards for the SDN's next phases, and whether K2 Space parlays its PTS-G bus work into a direct prime position on a future program.

The architecture is sound. Three overlapping layers — LEO data backbone