The math has been obvious for years. A Shahed-136 drone costs somewhere between $20,000 and $50,000 to manufacture. A Patriot interceptor costs roughly $3 million to $4 million per shot. Every time an adversary launches a swarm, they're printing money at the Pentagon's expense. The solution — high-energy lasers with a marginal cost measured in dollars, not millions — has existed in prototype form for over a decade. The problem was never the physics. It was the procurement logic that kept treating laser weapons like exotic research projects rather than production items.

That logic is now breaking down, and the pressure isn't coming primarily from inside the Pentagon. It's coming from a global arms race that isn't waiting for American institutional processes to catch up.

The Demand Signal Problem Hegseth Finally Named

Secretary of Defense Pete Hegseth's April 29 posture statement to the House Armed Services Committee was unusually candid about why directed energy has stalled. The statement acknowledged that the defense industrial base is "currently postured to produce only a limited number of prototypes" and identified the core dysfunction: manufacturers can't invest in production-scale manufacturing and supply chains if they can't predict how many systems they'll actually be asked to build. The Pentagon wants "tens to hundreds" of directed energy weapons. But wanting and signaling are different things, and the defense industrial base has learned — through decades of programs that peaked at prototype and then died — not to build capacity on the basis of aspirational statements alone.

Hegseth's framing is worth taking seriously precisely because it's self-critical. The statement doesn't blame the technology or the contractors. It names "business as usual acquisition mindset" and "institutional inertia" as the primary obstacles. That's a more honest diagnosis than most Pentagon budget documents offer. The question is whether naming the problem translates into fixing it — and the answer, historically, has been: not automatically.

What's different now is that the external pressure has become impossible to ignore. The demand signal problem is being solved, in part, by adversaries forcing the issue.

The UAE Convergence: What a Three-Laser Customer Reveals

The most clarifying data point in recent weeks didn't come from a Pentagon budget document. It came from the United Arab Emirates, which has somehow become the world's most instructive directed energy laboratory.

The Financial Times reported that Israel deployed a version of its 100-kilowatt Iron Beam laser to the UAE to help counter Iranian drone and missile attacks during Operation Epic Fury. Days later, a Chinese vehicle-mounted laser weapon — tentatively identified as consistent with the Guangjian-21A system — was spotted at Dubai International Airport. And a separate Congressional notification revealed the UAE had already requested to buy 10 American FS-LIDS counter-drone systems for $2.1 billion, with the command-and-control architecture specifically scoped to integrate a laser weapon being acquired through direct commercial sales.

Three laser systems. Two geopolitical blocs. One customer. One operational theater.

This is what an actual demand signal looks like — not a posture statement, but a government writing checks for multiple competing systems simultaneously because the threat is real and immediate. The UAE's procurement behavior is the clearest evidence yet that directed energy has crossed from "promising technology" to "operational necessity" in the minds of defense planners who are actually under fire.

For American defense startups, this convergence is both an opportunity and a warning. The opportunity: a proven, proliferating market for systems that work. The warning: the competition isn't just Lockheed and Raytheon anymore. It's Israel's Rafael and Elbit, it's Chinese state manufacturers, and it's European programs like the UK's Dragonfire. The window for American commercial defense tech to establish itself in this market is open — but it's not indefinitely open.

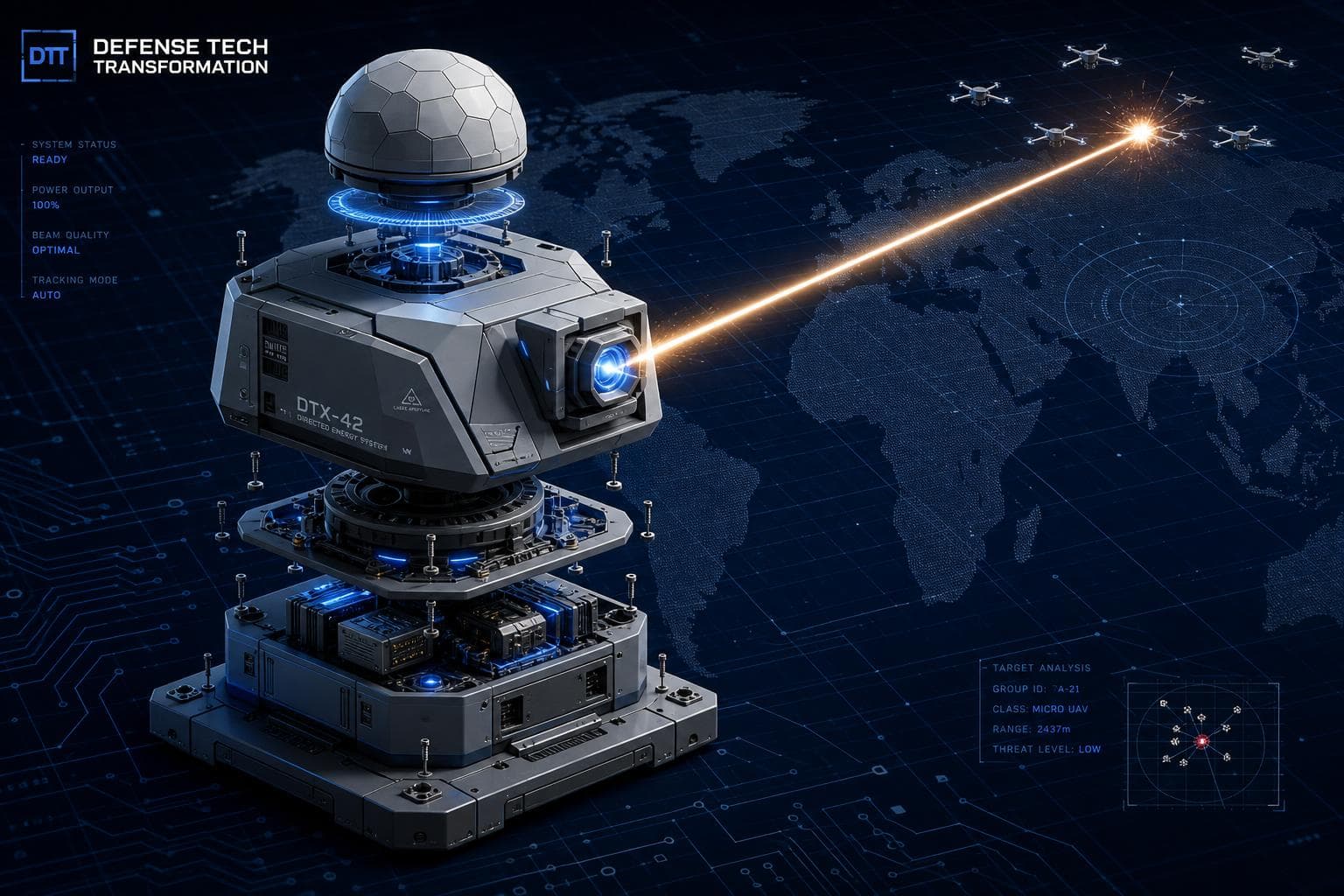

The $1.99 Shot and What It Actually Requires to Deliver It

The cost-per-engagement argument for directed energy is genuinely compelling. The National reported that operational laser systems are engaging drone targets at a cost of $1.99 per shot — a figure that, set against million-dollar interceptors, makes the economic case for laser air defense almost self-evidently obvious. A 100-kilowatt system with its own radar-based fire control can reportedly focus on a coin-sized area at 10 kilometers, engaging swarms in rapid succession.

But the $1.99 figure requires some unpacking, because it's the kind of number that can mislead as easily as it illuminates. The marginal cost of firing a laser is indeed negligible — you're paying for electricity. The capital cost of the system, its maintenance, its power infrastructure, its integration into existing command-and-control architecture, and its operator training are not negligible. The operational constraints are real: weather dependency, line-of-sight requirements, thermal management at sustained high power. These aren't dealbreakers, but they define where and how these systems can be deployed.

The more important point is what the $1.99 figure represents strategically. It means that once the capital investment is made, the cost curve inverts permanently. Every subsequent engagement gets cheaper relative to the adversary's cost to attack. That's a fundamentally different economic structure than any kinetic interceptor, and it's why the Pentagon's interest in scaling from prototypes to "tens to hundreds" of units isn't just about capability — it's about changing the underlying economics of air defense at scale.

The technology enabling this, at least in some of the most capable current systems, involves advances in beam combination and dynamic beam shaping. The National's reporting highlighted Civan Lasers' beam combination approach as enabling precise, microsecond energy control at 100 kilowatts — the kind of technical breakthrough that separates a laboratory demonstration from a system that can actually track and destroy a maneuvering drone in operational conditions.

Where Venture-Backed Startups Actually Fit in This Picture

The broader defense tech transformation context matters here. Based.info's analysis of the sector — drawing on reported figures — notes that defense-tech venture funding reached $49.1 billion in 2025, with equity funding more than doubling year-over-year. The companies capturing the most attention (Anduril, Shield AI, Palantir) are primarily winning on software-defined autonomous platforms, not directed energy hardware. Anduril's $20 billion Army contract is for Lattice integration. Shield AI's value proposition is Hivemind autonomy software. These are companies that scale through software margins, not through manufacturing laser emitters.

Directed energy is a different problem. It requires serious hardware manufacturing, power systems engineering, thermal management, and ruggedized integration — the kind of capital-intensive work that venture-backed startups have historically avoided because the margins look more like defense primes than software companies. The firms that have made the most progress — Raytheon's High Energy Laser with Integrated Optical-dazzler and Surveillance (HELIOS), Northrop's SHORAD programs — are legacy contractors with existing manufacturing infrastructure.

But the gap is narrowing, and it's narrowing in a specific way. The command-and-control and targeting software layer — the part that determines how a laser system identifies, tracks, prioritizes, and engages targets in a swarm environment — is exactly where software-native defense startups have an advantage. The UAE's FS-LIDS procurement specifically scoped C2 architecture to integrate a separately acquired laser weapon. That's a modular architecture, and modular architectures create entry points for companies that don't want to build the entire system.

The pattern emerging in directed energy mirrors what happened in drone warfare: hardware commoditizes over time, software and integration become the durable competitive advantage. The startups that figure out how to own the targeting and engagement logic layer — the "brain" of a laser air defense system — without having to manufacture the emitter will be positioned similarly to how Anduril positioned itself in autonomous systems: as the integrating intelligence rather than the commodity hardware.

The Procurement Reform Requirement Is the Real Bottleneck

Hegseth's posture statement was explicit that technology readiness isn't the binding constraint. The binding constraint is procurement process. The statement called for reforming "procurement processes, warfighting tactics, and policy limitations" to "demystify" directed energy and facilitate integration into force structure. That's a significant acknowledgment: the Pentagon is admitting that its own processes are the primary obstacle to fielding technology that works.

For startups, this creates a specific strategic problem. The demand signal is real — "tens to hundreds" of units is a genuine market if the procurement machinery can actually execute. But the history of directed energy programs is littered with systems that demonstrated capability, received enthusiastic endorsements from senior officials, and then stalled in the transition from prototype to program of record. The Laser Wars analysis noted that senior officials have been vocally endorsing laser weapons for years — "a laser on every ship" has been a recurring aspiration — without the institutional follow-through to match.

What's different now is the external forcing function. The UAE deployment, the Iranian drone campaigns, the Chinese export of laser systems to the Gulf — these aren't hypothetical threat scenarios. They're operational realities that are compressing the timeline for American decision-making. When adversaries are fielding and exporting directed energy systems in active conflict zones, the Pentagon's tolerance for multi-year prototype cycles shrinks considerably.

The companies best positioned to benefit aren't necessarily the ones with the most advanced laser technology. They're the ones that have already solved the procurement pathway problem — that have existing relationships with DIU, existing OTA contract vehicles, existing program-of-record experience that lets them move from contract award to fielded capability without getting trapped in the acquisition bureaucracy that has killed previous directed energy programs.

Watch for two specific indicators over the next six to twelve months: whether any directed energy system achieves program-of-record status under the FY2027 budget cycle (which would represent the institutional commitment that prototypes never received), and whether the C2 and targeting software layer for laser air defense systems starts attracting the kind of Series B and C venture investment that autonomous systems software attracted two years ago. The first would signal that Hegseth's demand signal has teeth. The second would signal that the startup community has identified the directed energy entry point that matches their actual competitive advantages.

The physics has been ready for years. The economics are now undeniable. The procurement machinery is the last variable — and it's finally under pressure from a direction the Pentagon can't ignore.